In recent years, we have witnessed the advent of a new India that is completely digital and is advocating for the growth of a cashless economy. People from all spheres of life embrace this digital change and acknowledge that it has made their lives much easier and more efficient. The increasing adoption of Unified Payments Interface (UPI) payment gateways has driven this change, encouraging this culture of cashless transactions and financial inclusion.

Now, let’s understand the details behind how the adoption of UPI payment gateways is turning out to be such a force in the growing digital economy of India, its impact on both individuals/businesses and how to choose the right provider for your UPI payment gateway integration.

What is UPI Payment Gateway?

Suppose there’s a marketplace, where instant transfers of money happen with just a tap and a PIN. This is the power of UPI-based payment gateways in India! Developed by the National Payments Corporation of India (NPCI), UPI stands for Unified Payments Interface. It’s a digital innovation that removes the need for cash and cheques, replacing them with a virtual payment address (VPA) linked to your phone number.

Think of a VPA as your personalized key to a digital vault. It enables instant money transfers from your bank account. But how does this process take place when it comes to transactions between merchants and customers? Here’s where UPI based payment gateways step in as the middlemen.

These gateways act like bridges, connecting your favorite UPI app (like PhonePe, Google Pay, MobiKwik or Paytm) to the merchant’s platform. The process is smooth and secure. When you make a purchase, the gateway initiates a request to your UPI app, specifying the exact amount. You then verify the transaction with your UPI PIN.

Once the PIN is verified, the gateway securely transfers funds from your bank account to the merchant’s. To keep everyone informed, the gateway provides transaction reports – a digital receipt for you and the merchant, confirming the transfer and its details.

So, the next time you make a purchase using UPI, remember that it all happens with the help of the UPI payment gateways.

Impact on Individuals

Rani, a young woman living in a metropolitan city in India, didn’t like mornings. The bus ride to work was always a struggle, crowded with people, and often she’d find herself empty-handed at the tea stall, having forgotten her wallet in a rush. But Rani then came to know about an alternative – UPI, short for Unified Payments Interface, which lets you transfer money directly, from the payer’s account to the payee’s account. And here’s the cool part: you don’t need to remember long account numbers. Instead, UPI uses a virtual payment address (VPA), which is basically a unique short alphanumeric combination assigned to your bank account.

Rani downloaded a UPI app like PhonePe or Google Pay. Now, Rani could simply scan a QR code at the tea stall or enter the vendor’s VPA on her phone, type in her UPI PIN, and voila!

But UPI wasn’t just for chai. Rani could send money to her brother back in the village with a few taps, pay her electricity bill, and even shop online for that beautiful saree she’d been eyeing. UPI made everything quicker, safer, and much more convenient.

UPI has empowered individuals like Rani in many ways:

- Convenience: UPI transactions are instant, eliminating the need to carry cash or visit ATMs. Payments can be made anytime, anywhere, with just a few taps on a smartphone

- Security: UPI utilizes robust PIN-based authentication, minimizing the risk of fraud compared to cash transactions

- Financial Management: UPI apps provide detailed transaction histories, allowing users to track their spending and manage finances effectively

- Accessibility: UPI has opened the doors to financial inclusion, particularly for those who lack access to traditional banking services. With a basic smartphone and bank account, anyone can participate in the digital economy

Impact on Businesses

Rani wasn’t the only one who loved UPI. Shopkeepers and other businesses loved it too. No more worries about fake cash or the hassle of giving change. Transactions were instant, and they could reach more customers who preferred to pay digitally.

Businesses of all sizes have gained significant benefits from UPI integration:

- Faster Transactions: UPI transactions are processed instantly, leading to quicker order fulfillment and improved customer experience

- Wider Reach: UPI caters to a vast customer base familiar with mobile payments, expanding the reach of businesses beyond traditional payment methods

- Reduced Operational Costs: UPI eliminates the need for cash handling and associated costs like managing physical cash or maintaining card terminals

- Enhanced Security: UPI’s secure architecture minimizes the risk of fraud compared to cash-on-delivery transactions

- Data-Driven Insights: Transaction data from UPI payments can provide valuable insights into customer behavior, aiding businesses in making informed decisions

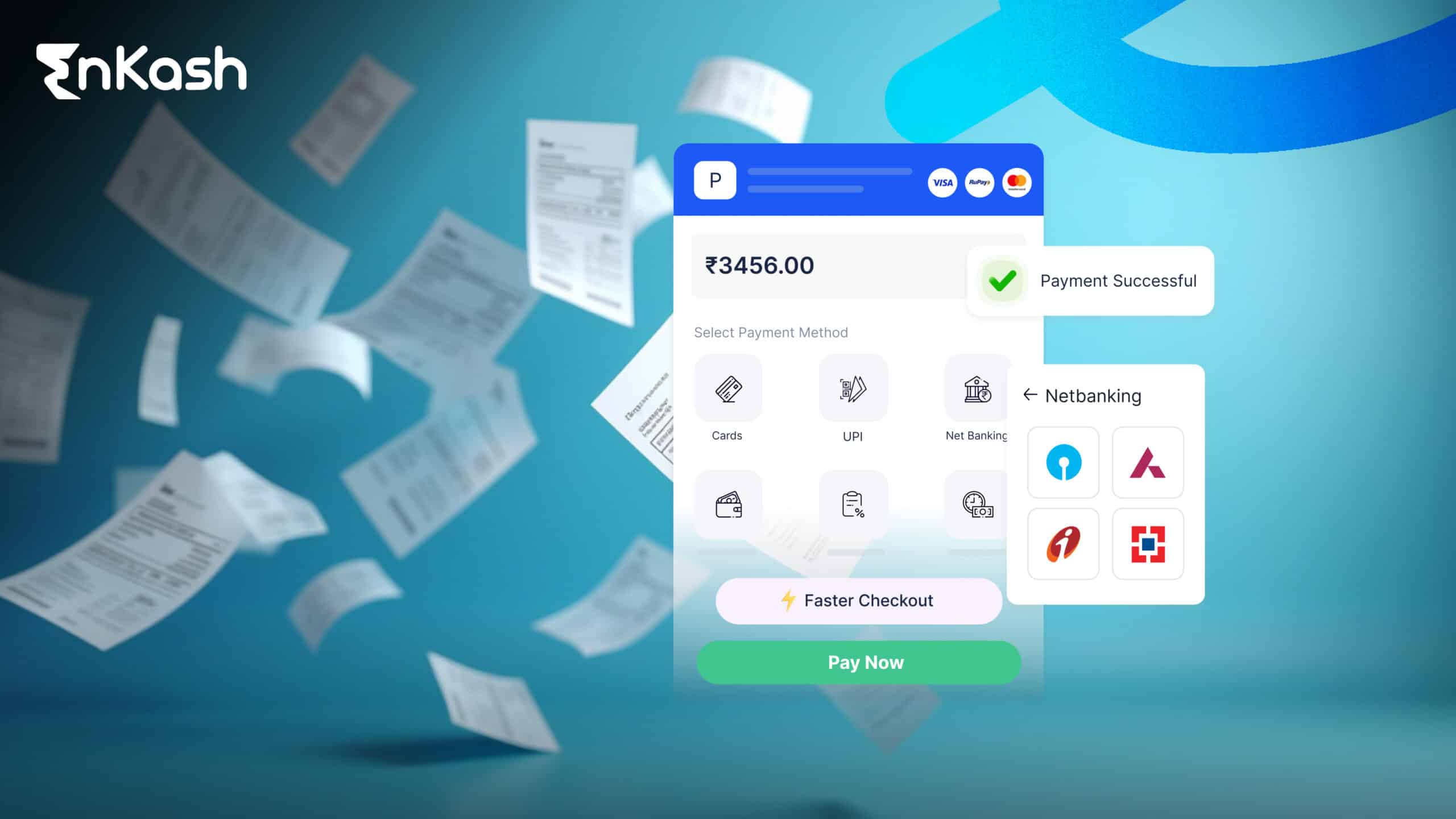

Types of UPI Gateway Integration

Now that we understand the advantages of UPI payment gateways for both individuals and businesses, let’s understand the different ways these gateways can be integrated:

Direct Integration: This method involves a business directly integrating the UPI gateway’s API (Application Programming Interface) into their website or app. This offers a high degree of customization but requires technical expertise and resources for development and maintenance.

Payment Link Integration: Here, the gateway generates a unique payment link for each transaction. Customers can access this link via email, SMS, or social media and complete the payment using their preferred UPI app. This method is simpler to set up but offers less customization compared to direct integration.

QR Code Integration: This is a widely used method where a QR code (Quick Response code) is generated for each transaction. Customers simply scan the QR code with their UPI app to initiate the payment. This is a quick and user-friendly option, perfect for in-store payments or displaying on product packaging.

Aggregator Integration: Businesses can leverage payment aggregators that offer pre-integrated UPI payment options. This is a hassle-free solution for businesses with limited technical resources, but transaction fees might be slightly higher compared to direct integration.

How to choose a provider for UPI Payment Gateway Integration?

Choosing the right provider for UPI payment gateway integration is crucial for your business success. Here are some key factors to consider:

- Transaction Fees: Compare the UPI payment gateway charges by different providers for each transaction. These fees may vary based on transaction volume and the chosen integration method

- Security Features: Ensure the provider offers robust security measures to protect sensitive customer data. Look for certifications like PCI DSS compliance, which indicates adherence to stringent data security standards

- Settlement Speed: Consider the time it takes for funds to be settled into your business account after a successful transaction. Faster settlements improve your cash flow

- Technical Support: Opt for a provider that offers reliable technical support to assist you with any integration or troubleshooting issues

- Brand Reputation: Choose a well-established provider with a proven track record of reliability and customer satisfaction

Learn More About How UPI Payments Can Grow Your Business

How Olympus Payment Gateway Can Help?

Olympus payment gateway is a product of EnKash, a leading provider of payment processing solutions in India. With Olympus payment gateway, you can get comprehensive support for UPI payments, enabling your business to take off by seamlessly integrating UPI payment gateways into your platforms. With Olympus, you can leverage the power of UPI to streamline your payment processes, enhance customer experience, and get exposure to reach a wider audience.

Final Note

UPI payment gateways have revolutionized the way Indians pay and get paid. Their impact on individuals, businesses, and the economy as a whole is undeniable. As UPI continues to evolve, it holds immense potential to further propel India towards a cashless, inclusive, and digitally empowered future.