Introduction

When GST was introduced in India in July 2017, the real adjustment began at the transaction level. We saw it in how invoices were raised, how returns were prepared, and how businesses had to reassess the way supplies were classified. GST brought different tax components into play depending on where a supply was made and how it was structured, and those distinctions started influencing everyday compliance decisions.

As businesses adapted, one pattern became clear. GST issues rarely stem from incorrect tax rates. They arise when a transaction is classified under the wrong GST component. Misreading whether a supply attracts CGST and SGST, UTGST, or IGST often leads to incorrect invoicing, credit mismatches, and reconciliation challenges.

This blog explains how GST components apply across common transaction scenarios. How you identify the correct tax, how revenue flows under each component, and how to avoid errors that typically surface during compliance and audits.

Objective of GST

The Goods and Services Tax (GST) was introduced in India in 2017 with the primary objective of simplifying the indirect tax system. It aimed to:

- Reduce Cascading Effect: Previously, several indirect taxes were levied at different stages of production and distribution, leading to a cascading effect that inflated the final price of goods and services. GST eliminates this by having a single tax point

- Promote Tax Compliance: A simpler tax structure with fewer exemptions makes GST easier for businesses to understand and comply with

- Boost Economic Growth: GST aims to encourage economic activity and growth by streamlining tax processes and reducing compliance burdens

- Create a Unified Market: GST facilitates the seamless movement of goods and services across states by eliminating inter-state tax barriers.

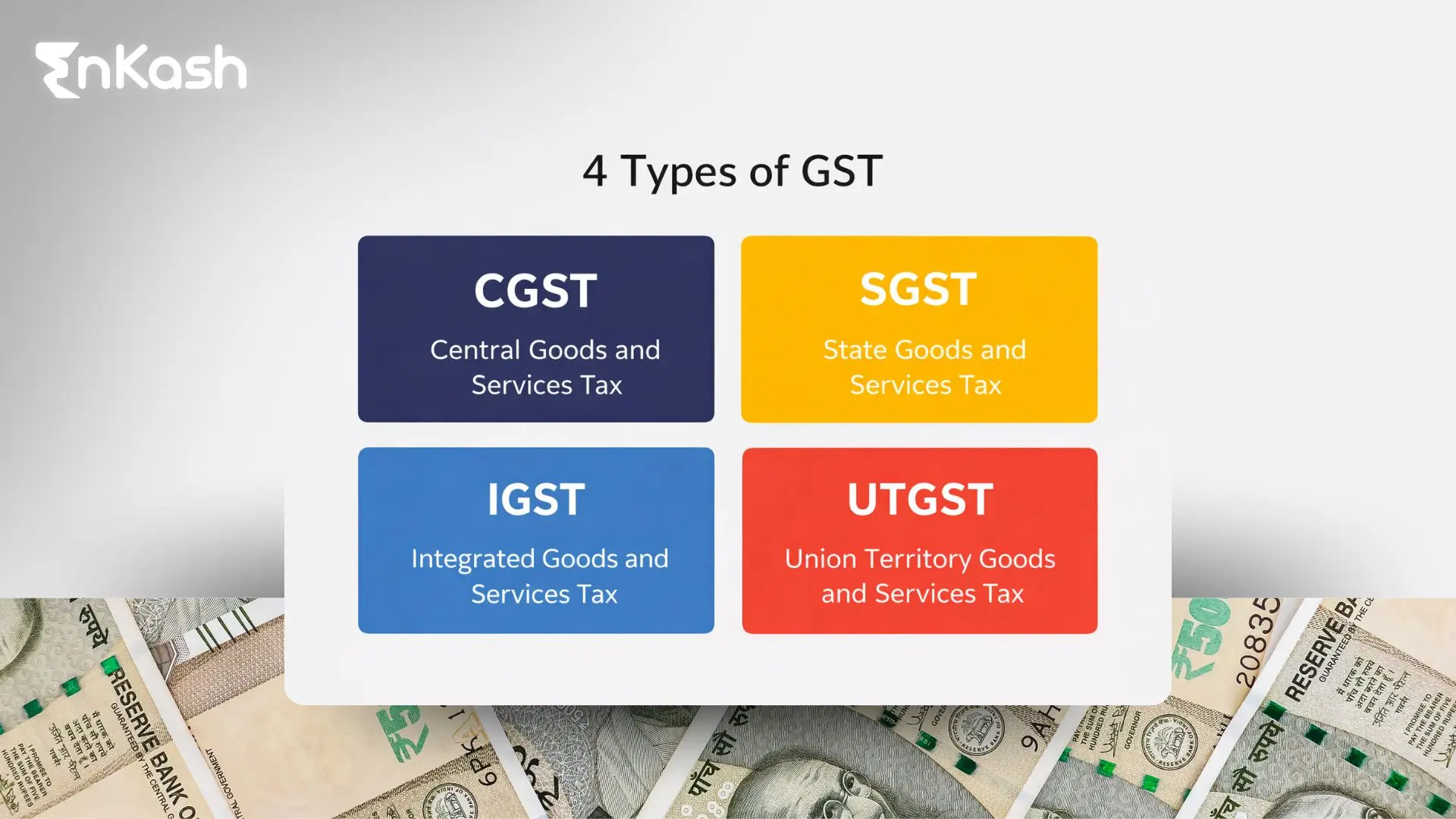

Types of GST in India

There are four main types of GST categories, which include Central Goods and Services Tax (CGST), State Goods and Services Tax (SGST), Union Territory Goods and Services Tax (UGST), and Integrated Goods and Services Tax (IGST).

There are four main types of GST categories, which include Central Goods and Services Tax (CGST), State Goods and Services Tax (SGST), Union Territory Goods and Services Tax (UGST), and Integrated Goods and Services Tax (IGST).

GST Type |

Description |

Applicability |

Collected By |

|---|---|---|---|

Central Goods and Services Tax (CGST) |

Imposed by the central government on the sale of goods and services within a single state. |

Applies within a state |

Central Government |

State Goods and Services Tax (SGST) |

Levied by the state government on intrastate transactions of goods and services |

Applies within a state |

State Government |

Union Territory Goods and Services Tax (UTGST) |

Functions similarly to SGST, but is applicable within Union Territories. |

Applies within a union territory |

Union Territory Government |

Integrated Goods and Services Tax (IGST) |

Levied on interstate transactions of goods and services, and also applies to imports and exports |

Applies between states or for import/export |

Central Government |

What is IGST?

Integrated Goods and Services Tax or IGST is an important component of India’s GST system which is applied to inter-state transactions, imports and exports.

It is charged by the Central Government and further distributed between the Centre and the respective State where goods and services are being consumed.

IGST is the combination of the Central GST (CGST) and State GST (SGST) components as the total rate is equal to the sum of CGST and SGST rates.

Features of IGST

Interstate Transactions

IGST is applicable to all transactions involving the supply of goods and services across state borders on imports and exports.

Imposed by the Central Government

IGST is imposed and administered by the Central Government. However, the revenue is shared between the State and the Central governments.

Destination-Based Taxation

IGST is collected and passed on to the state government where the goods or services are finally consumed, and not where they were orignally produced.

Simplified Compliance

IGST dismisses the need for separate tax filings for interstate transactions, eliminating the compliance burden on businesses.

Rate Structure

The IGST rate is usually equal to the sum of the Central GST (CGST) and State GST (SGST) rates.

How to calculate IGST

GST calculation is pretty simple and requires an easy formula. Let us understand it better with an example.

Formula to Calculate IGST

IGST = Taxable Value × IGST Rate

Example of IGST Calculation

Suppose there is a product valued at ₹10,000. So, the GST applicable on it would be 18%. IGST would also be the same.

GST rate = 18% (so IGST = 18%)

IGST = 10,000 × 18% = ₹1,800

Total invoice value = ₹11,800

Now this ₹1,800 will be divided between Central and the respective State government where the product has been supplied.

Why was IGST introduced?

IGST was introduced to curb the gap in India’s old indirect tax system, or rather simplify it. Before IGST there were multiple taxes like VAT, CST and entry tax often creating confusion and delays at state borders. There was no proper input tax credit across states before IGST.

IGST Applicability

IGST is applicable under following situations:

- When the seller and buyer are in different states

- When goods and services are imported from outside the country

- When goods and services are exported from the country

- When same company has different GST registrations

- When an ecommerce platform facilitates interstate transactions

IGST Rate Structure

IGST rates are same as the GST structure. Follow the table below to know the tax slabs.

IGST Rate |

Goods/Services |

Examples |

|---|---|---|

0% |

Necessary goods & zero-rated supplies |

Fresh fruits, vegetables, exports |

5% |

Essentials |

Packaged food, transport services |

12% |

Standard goods |

Processed food, mobile phones |

18% |

Most commonly used standard rate |

Electronics, standard restaurants |

28% |

Luxury goods |

Cars, ACs, premium items |

Central Goods and Services Tax (CGST)

Central Goods and Services Tax (CGST) is the portion of GST collected by the Central Government on intra-state supplies of goods and services in India. It is governed by the Central Goods and Services Tax Act, 2017, which lays down the legal framework for levy, collection, compliance, input tax credit, and enforcement.

CGST forms one-half of the tax charged on transactions that take place within the same state, with the other half being SGST (or UTGST in certain Union Territories).

When is CGST Applicable?

CGST applies when the location of the supplier and the place of supply are in the same state or Union Territory. In this scenario, the total GST rate is divided equally between the Centre Government and the State Government.

Example:

If a business operates in Haryana and sells goods worth ₹1,00,000 within Haryana, and the GST rate is 18%:

- 9% CGST → ₹9,000 (paid to the Central Government)

- 9% SGST → ₹9,000 (paid to the Karnataka State Government)

CGST is an important pillar of India’s dual GST model, which is designed to create a balanced tax-sharing system between the Centre and State governments while ensuring a destination-based tax regime. For businesses operating within a single state, CGST compliance directly affects cash flow, credit eligibility, and audit risk, making accurate classification and financial reporting essential.

State Goods and Services Tax (SGST)

State Goods and Services Tax (SGST) is the state component of India’s dual GST system, levied by the respective State Government on the intra-state supply of goods and services. It is governed by the individual State GST Acts, 2017, which operate in coordination with the CGST Act to ensure a unified but dual tax structure across India.

SGST represents the share of GST revenue that belongs to the state where the goods or services are consumed, reinforcing the destination-based taxation principle of the GST regime.

When is SGST Applicable?

State Goods and Service Tax (SGST) is charged when the supplier and buyer are located in the same state, and the place of supply is within that state. In such transactions, GST is divided equally between CGST and SGST.

Example:

A supplier in Tamil Nadu sells goods within Tamil Nadu at an 40% GST rate:

- 20% CGST → Paid to the Central Government

- 20% SGST → Paid to the Tamil Nadu State Government

SGST is not just a tax component; it is a critical part of India’s fiscal federal structure under GST. Businesses operating within a single state must manage SGST carefully to maintain credit efficiency, ensure regulatory compliance, and avoid working capital blockages caused by incorrect tax classification.

Union Territory Goods and Services Tax (UTGST).

Union Territory Goods and Services Tax (UTGST) is the Union Territory–level component of India’s GST system, levied on intra-Union Territory supplies of goods and services in Union Territories without a legislative assembly. It is governed by the Union Territory Goods and Services Tax Act, 2017.

UTGST functions similarly to SGST but applies specifically to certain Union Territories, ensuring tax revenue is allocated to the respective UT administration under India’s destination-based GST framework.

Where is UTGST Applicable?

UTGST applies in Union Territories without a legislature, currently including:

- Andaman and Nicobar Islands

- Lakshadweep

- Dadra and Nagar Haveli and Daman and Diu

- Chandigarh

In these territories, GST on intra-UT transactions is split into:

- CGST (Central share)

- UTGST (Union Territory share)

Union Territories with legislatures, such as Delhi, Puducherry, and Jammu & Kashmir, follow the SGST model, not UTGST.

UTGST revenue collected from intra-UT supplies is assigned to the respective Union Territory administration, forming an important source of indirect tax revenue for governance and public services in those territories.

GST Tax Comparison: Intra-State vs Inter-State

Feature |

CGST / SGST / UGST (Intra-state) |

IGST (Inter-state / Import-Export) |

|---|---|---|

Taxing Authority |

Central (CGST) + State/UT (SGST/UGST) |

Central only (IGST shared with State as per destination) |

Applicability |

Within the same State or UT |

Between States, or State ↔ UT, imports/exports |

ITC Utilisation |

Separate CGST & SGST/UGST credits |

IGST credit usable across CGST & SGST/UGST liabilities |

2025 Key Changes |

Hard-locking of GSTR-3B, e-Way Bill 2.0, MFA, and ISD mandates |

Auto tax-split via GSTN, stricter place of supply compliance |

The payment of GST on time is of great importance to any business. Failure to do so can result in penalties and statutory compliance issues. Often, companies face issues retrieving the amount to be paid from the portal and then going through the process of making the challan, checking it, and getting the approvals internally to make the payment.

That is where a platform like the one we offer to our customers at EnKash helps you. You can set maker, checker, and approver levels within the tax payments module so that once you retrieve the amount to pay, you can get the requisite approvals in place.

Moreover, you also have various payment options to complete the payment via the portal. Once the payment is completed, your finance system is updated automatically.

Difference between CGST, SGST, UTGST & IGST

Aspect |

CGST |

SGST |

UTGST |

IGST |

|---|---|---|---|---|

Full form |

Central Goods and Services Tax |

State Goods and Services Tax |

Union Territory Goods and Services Tax |

Integrated Goods and Services Tax |

Levied by |

Central Government |

State Government |

Central Government (for applicable Union Territories) |

Central Government |

Applies to |

Intra-state supplies |

Intra-state supplies |

Intra-Union Territory supplies (in UTs without a legislature) |

Inter-state supplies, supplies between State and Union Territory, and imports |

When it is charged |

Along with SGST or UTGST on the same invoice for intra-state / intra-UT transactions |

Along with CGST on the same invoice for intra-state transactions |

Along with CGST on the same invoice for applicable intra-UT transactions |

As a single tax on inter-state / inter-UT transactions and imports |

Who receives the revenue |

Central Government |

Respective State Government |

Union Territory administration (via the UTGST framework) |

Collected by the Centre and later settled to the destination (consuming) State/UT as per the IGST settlement mechanism |

Administration |

Central Board of Indirect Taxes and Customs (CBIC) |

Respective State GST / State Tax Department |

GST authorities for the applicable Union Territory |

Administered under the GST framework (Centre and States coordinate for settlement) |

How can Businesses Claim Input Tax Credit (ITC) on IGST

When you pay IGST on interstate purchases, you can claim it as credit and use it to reduce your tax liability on sales.

You can claim ITC only if:

✔️ You have a valid tax invoice

✔️ You have received goods/services

✔️ The supplier has filed GST returns (GSTR-1)

✔️ The ITC reflects in your GSTR-2B

✔️ You have filed your GSTR-3B

✔️ The payment to supplier is made within 180 days

IGST Refund

When the ITC claim by a b2b buyer is higher than the GST liability, that is when IGST refund becomes necessary. This situation usually occurs in the export business. The tax liability on exports is NIL when used an Letter of Undertaking.

Conclusion

GST becomes manageable when we apply its components with clarity. CGST, SGST, UTGST, and IGST exist to ensure tax is collected by the right authority based on where a supply is made and where it is consumed. Once we identify the location of the supplier and the place of supply correctly, the applicable GST component is no longer a guess.

Across intrastate, interstate, Union Territory, and import transactions, the structure stays consistent. What changes is how the tax is applied, collected, and settled. In our experience, most GST issues do not start with tax rates. They begin when a transaction is classified under the wrong component, and that mistake then carries forward into invoicing, credit utilisation, and reconciliation.

Have more questions related to GST? You can find those answers here.

FAQs

What is GST, and when was it implemented in India?

GST is an indirect tax system implemented in India on July 1, 2017, replacing multiple indirect taxes.

What are the main components of GST?

GST operates through four components:

- Central Goods and Services Tax (CGST)

- State Goods and Services Tax (SGST)

- Union Territory Goods and Services Tax (UTGST)

- Integrated Goods and Services Tax (IGST)

Each component applies based on where a supply takes place and which authority is entitled to collect the tax.

When do CGST and SGST apply?

CGST and SGST apply when the location of the supplier and the place of supply are within the same state. Both components are charged on the same transaction, with CGST collected by the Central Government and SGST collected by the respective State Government.

Is the GST rate different for CGST, SGST, UTGST, and IGST?

No. The overall GST rate remains the same. What changes is how the tax is split. For example, an 18% GST rate may be split into 9% CGST and 9% SGST or UTGST, or applied as 18% IGST, depending on the transaction type.

How do we decide which GST component applies to a transaction?

The applicable GST component is determined by identifying two factors: the location of the supplier and the place of supply. Once these are established, the transaction is classified as intrastate or interstate, and the correct GST component follows.

Does IGST apply only to imports?

No. While IGST applies to imports, it also applies to supplies made between different states and between states and Union Territories. Imports follow the same interstate treatment under GST.

When is IGST charged?

IGST applies when a supply crosses state or Union Territory boundaries. This includes interstate supplies, supplies between a state and a Union Territory, and imports of goods or services. IGST is charged as a single tax and later settled with the destination state or Union Territory.