For organizations seeking to simplify their payment processes, it’s essential to be aware of the difference between a payment gateway and a payment processor. The payment gateway acts as a front-end payment interface that facilitates a secure, convenient payment setup. A payment processor, in contrast, takes care of the back end, securely moving information between banks, card networks and merchants. Together, they create the foundation of effective online payments and allow businesses to provide an enhanced user experience.

Introduction

In the fast-growing digital economy, electronic payments are the foundation of modern commerce, enabling companies to service the needs of an international and cashless marketplace. Whether it is online shopping, subscription services, or big corporate purchases, the need for safe, secure, and convenient payment channels has never been more pressing. Payment gateways and payment processors, two elements in this ecosystem that make transactions fast and safe, are central to it.

While interacting with each other, payment gateways and processors play different roles. The failure to understand their role can lead to operational inefficiencies, increased costs and security risks. Therefore, it is important for companies to understand their individual roles. This blog will cover all the major differences, functions and uses of payment gateways and payment processors to help businesses enhance their payment strategies, increase customer satisfaction, and remain competitive in an ever-changing online marketplace.

What is a Payment Gateway?

A payment gateway is the front-end technology that businesses use to accept electronic payments securely. It serves as the mediator between the customer and the payment system, making sure that confidential payment data is protected and encrypted.

Key Features of Payment Gateways

- Encryption: Ensures that the payment data from the customer (such as credit card numbers) is protected.

- Fraud Detection: Detecting suspicious activity to stop unauthorized payments.

- Ease of Use: Creates a seamless experience for users to pay.

- Multi-Currency Support: Supports international trade by supporting multiple currencies.

- Custom Integrations: Provides companies the ability to link the gateway with their platforms to give customized experience.

Role in Digital Transactions

The payment gateway takes payment information and securely transmits it to the payment processor for authentication. Without it, merchants cannot offer a user-friendly and secure way for customers to make payments. Additionally, payment gateways usually include analytics, which allows organizations to see payment trends and problems.

What is a Payment Processor?

A payment processor sits behind the scenes doing the complex work needed to settle a payment. It connects merchants to card networks, banks and other financial institutions to facilitate the flow of funds.

Key Features of Payment Processors

- Data Transmission: Conveys customer information safely from one end of the transaction to another.

- Authorization: Determines if a customer has enough funds or credit to make a payment.

- Settlement: Enables money to be transferred from the customer’s account to the merchant’s account.

- Chargeback Management: Manages disputes when customers request a refund from their banks.

- High Transaction Speed: Processes payments quickly, decreasing wait times for both merchants and consumers.

Importance in Payment Systems

The payment processor does the necessary work to have transactions approved, verified and cleared in a timely manner. Companies cannot make electronic payments if they do not have a processor, and it is an essential part of payment solutions. These days, processors also often use AI to detect fraud to make them more reliable and secure.

Constituents of Electronic Payment

Electronic payments need multiple interdependent parts to operate effectively, safely and securely. Knowing these constituents helps businesses get a grasp on the payment landscape.

Key Components

- Payment Gateway: Provides the mechanism for the transaction to take place.

- Payment Processor: Runs the back-end functions to process the payment.

- Merchant Account: A specialized account where funds from card payments are deposited.

- Customer Interface: The platform where customers input their payment details.

- Security Protocols: Encryption, tokenization, and fraud detection systems are used to secure the transaction.

- Regulatory Compliance Tools: Ensures adherence to legal standards such as PCI DSS and AML guidelines.

Together these parts form a unified payment infrastructure, enhancing the efficiency of businesses and customers in conducting transactions and protecting sensitive information.

Key Differences Between Payment Gateway and Payment Processor

Introduction to Key Differences

Payment gateways and payment processors are part of the same infrastructure to facilitate electronic payment but have their own distinct functions. It is important to learn these differences so that businesses can implement these tools in a way that best fits their needs.

Comparison Table

Feature |

Payment Gateway |

Payment Processor |

Functionality |

Acts as the customer-facing interface that collects and securely transmits payment information. It enables users to input card or payment details through a secure platform. |

Operates in the background to facilitate the validation, authorization, and settlement of payments between banks and merchants. |

Role |

Encrypts sensitive payment data and ensures it is securely transmitted to the processor for further action. Provides additional features like fraud detection, recurring billing, and multi-currency support. |

Communicates with issuing banks, card networks, and acquiring banks to authorize and settle the transaction. Plays a critical role in ensuring funds are transferred to the merchant\u2019s account efficiently. |

User Interaction |

Visible to the customer and designed to be user-friendly, ensuring seamless payment experiences during the checkout process. |

Invisible to the customer, handling back-end tasks like error checks, fund validation, and dispute resolutions. |

Security Measures |

Focuses on front-end security with encryption, tokenization, and compliance with standards like PCI DSS. Integrates real-time fraud detection tools to safeguard customer data. |

Ensures secure communication between financial institutions and compliance with regulatory standards to prevent fraud and data breaches. |

Cost |

May include subscription fees, per-transaction costs, and additional charges for premium services like analytics and fraud prevention. |

Typically charges per transaction, along with potential fees for high-volume processing and chargeback management. |

Customization |

Allows businesses to customize checkout interfaces and payment flows to suit customer preferences and branding. |

Limited to back-end operational efficiencies, ensuring smooth data transmission and settlement without direct customization options. |

With a close look at these differences, companies can better match their payment architecture to their business objectives, which will boost efficiency and customer satisfaction.

When to Use a Payment Gateway vs. Payment Processor

It can be a difficult task for a company to decide whether it is a payment gateway or a payment processor, or both. It depends on what sort of transactions they process and the infrastructure they need. With the knowledge of their specific needs, companies can design their payment system in a way that supports both business goals and customer expectations.

When to Use a Payment Gateway

Payment gateways work best for companies that focus on customer engagement and frictionless payment methods. Key scenarios include:

- E-commerce Platforms: Online shops that require easy checkout will be using payment gateways to ensure a smooth customer experience.

- Subscription-Based Services: Recurring billing companies like streaming service providers or SaaS firms rely on gateways to securely process monthly or annual payments.

- Mobile and Web Applications: Payment-based apps and websites have direct access to gateways that provide optimized interfaces for a smooth user experience.

- Global Expansion: Companies expanding to global markets implement multi-currency support gateways so that the customer can pay using the local currency.

- Customer Analytics: Gateways offer the opportunity to gain insights into payment trends, which enables businesses to tweak strategies and increase customer satisfaction.

When to Use a Payment Processor

You’ll need a payment processor to handle the technical and logistical aspects of payments. Key use cases include:

- High-Volume Businesses: Organizations that handle large volumes of data, like retail chains or marketplaces, require processors to efficiently process the data.

- Point-of-Sale (POS) Systems: Physical stores use processors to link card terminals to financial networks.

- Quick Fund Settlement: Processors facilitate quick fund payments that are essential for managing cash flow in the hospitality and logistics sectors.

- Dispute Resolution: Processors have a central role in handling chargebacks and refunds, which reduces the amount of risk for merchants.

- Time-Sensitive Transactions: Services such as travel and ticketing require high-speed processing to fulfil customer needs.

Streamlining Payment Systems

Businesses can pick between a payment gateway, a payment processor, or a combination of both by carefully analyzing their needs and transactions. For instance, a small online shop can use a single system, whereas a big chain may need individual systems depending on its size. Payment tools that match business objectives not only lower costs, but improve customer satisfaction and loyalty.

How Payment Gateways and Processors Work Together

The interconnectedness between payment gateways and payment processors is a critical part of electronic payments. Every part is important to make every payment safe, reliable, and efficient. This integration allows enterprises to process transactions efficiently and meet customer needs.

Step-by-Step Payment Flow

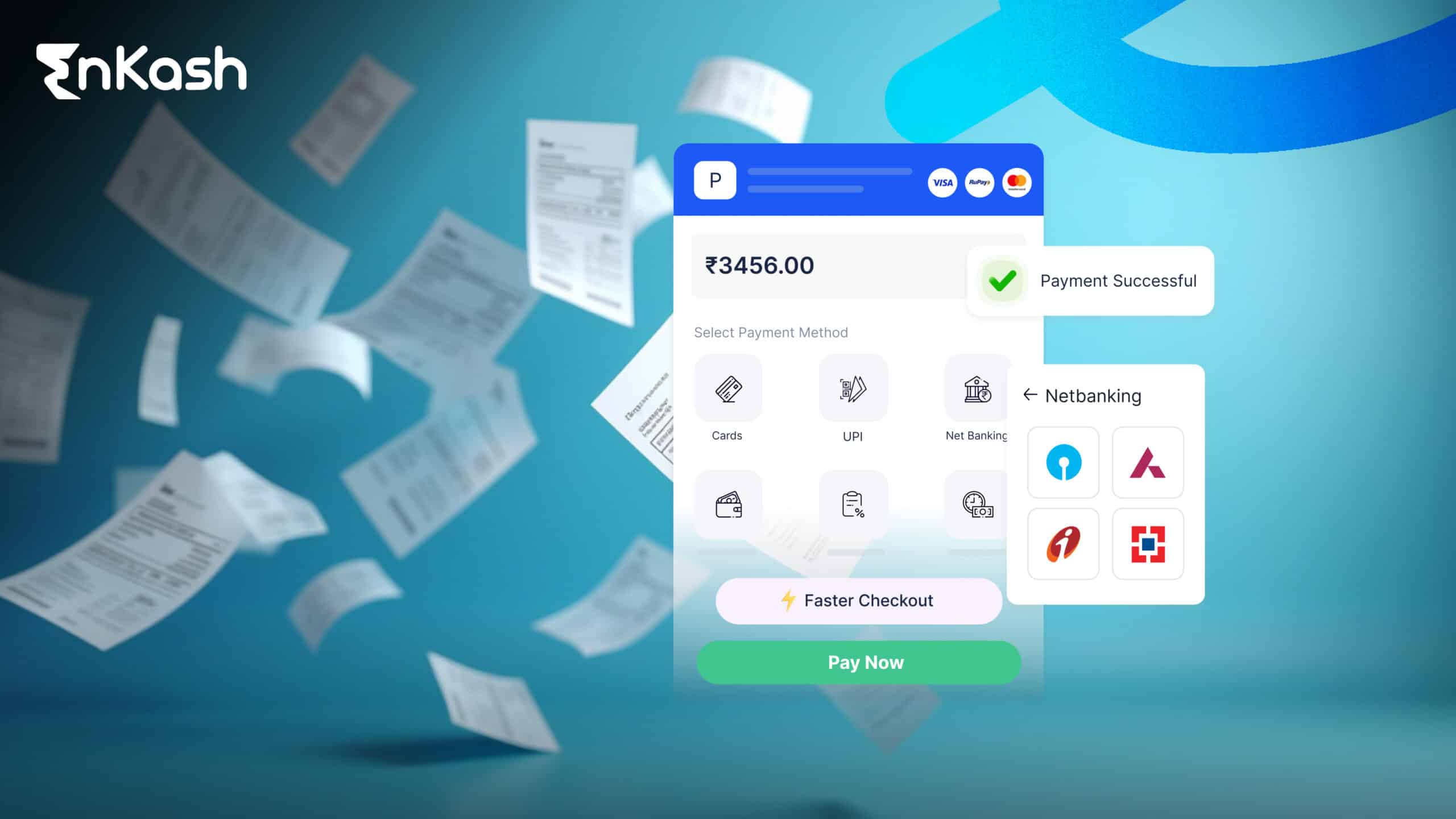

- Customer Inputs Details: Payment begins when a customer enters their payment information on the gateway page, which is secure and easy to navigate.

- Data Encryption: The gateway encrypts the payment data to keep it out of the hands and avoid unauthorised sending.

- Processor Validation: Once encrypted information reaches the processor, it relays information to banks, card networks, and other financial organizations in order to verify the transaction.

- Authorization: The processor approves or denies the payment depending on available funds and other factors.

- Settlement: For credited transactions, the funds are deposited from the customer’s bank account into the merchant’s account, and the transaction is complete.

Enhanced Features in Modern Systems

Most modern payment systems are built with things such as real-time notifications and status messages, which help businesses and users track transactions. They add to transparency and trust because both sides are aware of where the transaction is.

Importance of Collaboration

Gateways and processors work together to make payments fast, secure and frictionless. For enterprises, this partnership reduces mistakes, speeds up transactions, and provides a seamless payment experience, which increases customer satisfaction and business effectiveness.

Common Challenges and Solutions

Payment gateways and processors are very beneficial, but they can be difficult to implement for businesses. Recognizing these limitations in advance will allow companies to plan on how to overcome them and make payments smooth and easy.

Key Challenges

- Integration Complexity: Companies often find it difficult to integrate payments with their current platform. Customization and compatibility issues can cause deployment delays and impact the user experience.

- Cost Management: Advanced options like fraud detection and multi-currency integration can be costly. Monthly subscription fees, per-transaction fees, and hidden costs all eat up money for small businesses.

- Compliance: Compliance is essential, but it is often hard to comply with regulatory requirements such as PCI DSS or AML standards. Failure to comply means prosecution and data theft.

- Fraud Risks: Cyber threats are always evolving, so fraud prevention needs to be constantly upgraded. Without being able to keep ahead of these risks, you risk losing your business and losing your reputation.

Solutions

- Trusted Providers: Choose reliable payment service providers that provide robust integration and scalable solutions for your business.

- Scalable Pricing Plans: Choose plans tailored to transaction volumes and business growth. Transparent pricing can help manage costs effectively.

- Regular Audits: Perform regular audits to check if the organization is adhering to regulatory guidelines and identify gaps in service.

- AI-Driven Security: Leverage advanced fraud detection tools powered by AI to identify and mitigate potential risks proactively.

By dealing with these issues properly, organizations can increase efficiency, provide safe payment methods and earn customer trust. The first step in identifying and solving payment issues opens the path to development and long-term success.

Conclusion

It’s essential for businesses to know the importance of payment gateways and payment processors in order to manage their payment processes and improve productivity. Payment gateways act as the front-end interface to securely and easily initiate transactions, whereas payment processors perform the back-end functions of validation, authorisation, and payment settlement. They provide an ecosystem for processing electronic payments across multiple industries.

For organizations, understanding what their payment ecosystem needs is key to the choice of tools and vendors. The strategic pairing of payment gateways and processors not only helps to increase transaction security but also increases customer satisfaction and scalability. Furthermore, you’ll need to stay abreast of trends like AI-based fraud detection and blockchain technology to be able to maintain a competitive edge.

In this ever-changing world of payments, organizations need to keep up with the technological trends and focus on compliance with regulations. That way, they can secure their payments in the future, build customer trust, and achieve sustainable growth in an ever-digital economy.

FAQs

How does a payment gateway enhance customer trust in online transactions?

A payment gateway improves trust by providing a safe transaction environment using encryption and tokenization to secure payment information. In addition, capabilities such as real-time fraud detection and PCI DSS compliance help customers know that their data is safe when they shop online.

What types of businesses benefit most from using a payment processor?

Transaction processing is particularly helpful to high-volume companies, such as retailers, travel agencies, and marketplaces, that can scale their business by using payment processors to efficiently process large volumes of transactions. In addition, businesses that need to process funds rapidly or face frequent chargebacks depend on processors to maintain smooth operations.

Are there alternative payment solutions besides gateways and processors?

Yes, there are options like payment aggregators and peer-to-peer payments. Aggregators combine payments across merchants, and peer-to-peer platforms offer direct payment without a merchant account. These are best for small enterprises or start-ups with limited infrastructure.

How do payment gateways handle cross-border transactions?

Payment gateways can make cross-border payments by facilitating multi-currency payments and adhering to international payment regulations. They collaborate with worldwide payment processors and banks for easy funds transfers and also provide foreign currency conversion and fraud prevention services for foreign clients.

What should a business consider when choosing a payment gateway?

Main priorities are integration with current platforms, transaction fees, security, customer support, and multi-currency support. Organizations must also review the user interface of the gateway to make their customers feel at ease.

How do payment processors help with chargeback disputes?

Payment processors help collect transaction information and work with banks to settle conflicts. They retain records of the transaction, which allows merchants to build a stronger argument when chargebacks are resolved, thereby eliminating any loss.

Can payment systems integrate with emerging technologies like blockchain?

Modern payment platforms can be linked to blockchain technology for transparency and security. Blockchain ensures permanent records of the transactions and can support decentralized payment networks, providing greater security to organizations and customers.

What role does customer analytics play in payment gateways?

Payment gateway customer analytics provides data about purchases, transactions, and payment preferences. Such information enables companies to fine-tune their marketing strategies, streamline the checkout experience, and retain customers by providing personalized experiences.

How do small businesses benefit from all-in-one payment solutions?

These solutions offer gateway and processor functionality together, which makes it easy for small enterprises to handle payments. Such products provide easy onboarding, lower setup fees, and a simple interface, enabling small businesses to get on with expansion without having to manage complex payments.

What future trends could redefine payment gateways and processors?

Future developments such as AI fraud detection, biometric authentication, and tokenized payments are likely to transform the payment landscape. They will bring security, efficiency, and the ability to keep up with customer demands to keep organizations on top of digital business.

How do payment gateways improve conversion rates for e-commerce businesses?

Payment gateways increase conversion rates by delivering a simple, intuitive checkout experience, integrating multiple payment types, and making transactions fast. Mobile-friendly UIs, One-click payments, and Guest Checkouts minimize cart abandonment and increase the customer experience.

What is the difference between hosted and non-hosted payment gateways?

Hosted gateways move users to a third-party platform to make the payment. They’re extremely secure but don’t have control over the user experience. Non-hosted gateways, however, process payments on the company’s site and give you more branding options but require stronger security and compliance.