Online payment technology serves as a basic element for e-commerce because customers use it to shop every day in our digital world. When companies move their operations online, they place payment protection first. With the rise in cybercrime, guaranteeing that online commerce is safe and secure is paramount. Therefore, a secure online transaction requires strong protection against these cyberattacks and identity theft problems. 3D Secure technology now provides stronger protection for payments made online through its special authentication protocol.

Our exploration will explain how 3D Secure affects payment gateways while explaining 3DS payment features and 3DS authentication steps. Our analysis will explore how 3D Secure developed over time and explain its security advantages and technical hurdles while showing how 3DS transactions beat previous methods in fighting fraud and supporting users.

What is 3D Secure?

3D Secure offers an advanced security protocol that safeguards online card payments with an added verification step. Visa created 3D Secure in 1999 as a way to fight growing fraud risks in online payments. The security system verified that the person making the purchase was the official cardholder. The transition of 3D Secure brings revolution to the world of 3DS payments when compared to their predecessors, focusing more on the ability to reduce fraud, improve user experience, and meet regulatory requirements.

The name “3D Secure” refers to the three domains involved in the authentication process: The authentication process takes place across three key domains known as Acquirer Domain, Issuer Domain, and Interoperability Domain. The different security domains work together to protect the payment experience from start to finish. The Acquirer Domain represents payment service providers and merchants who receive payments. At the same time, the Issuer Domain stands for the bank that issued the card, and the Interoperability Domain serves as the connection bridge between them using card networks like Visa, MasterCard, or American Express. Thus, one of the most influential advancements in the online payment business has been the introduction of 3D Secure (3DS), an authentication protocol designed to provide an extra layer of protection during online credit and debit card transactions.

Read more: Cost control

How does 3D Secure work?

The core purpose of 3D Secure is to make sure that the cardholder has valid ownership rights to the mentioned card before completing the whole online transaction.

The procedure concerns multiple steps:

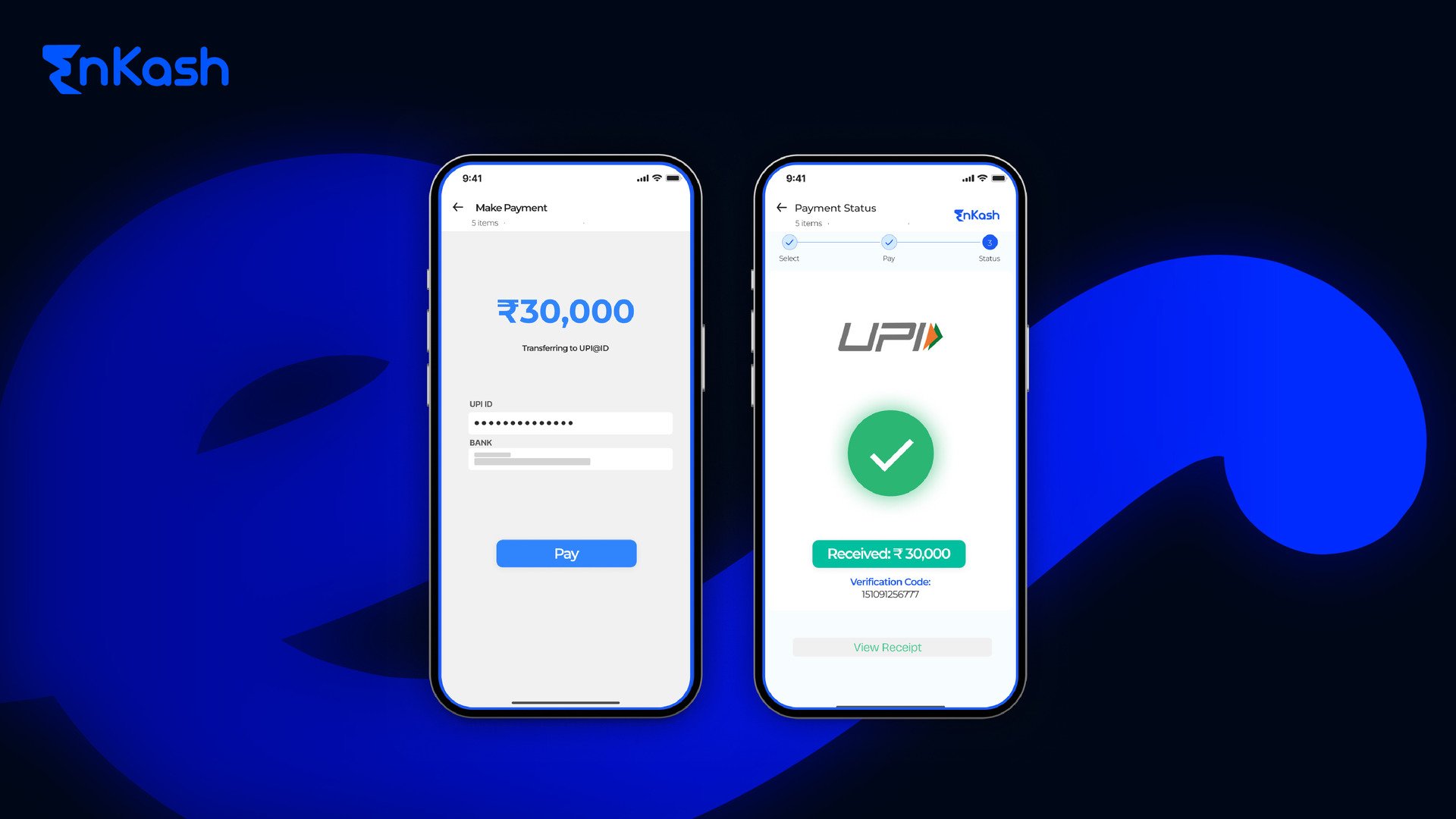

- Transaction Initiation: Customers begin purchasing when they enter their payment card details on a merchant website.

- Registration Check: The payment gateway confirms if the card belongs to the 3D Secure program before moving the transaction forward.

- Redirect to Authentication Page: When a customer uses an enrolled card, they get redirected to the 3D Secure authentication page of their card issuer to verify their identity by using a one-time passcode (OTP) sent to their phone.

- Authentication: Customers must present their OTP or unique password for identity verification before they can restart their purchase.

- Transaction Completion: The customer returns to the merchant’s website once they finish payment processing through 3D Secure security checks.

3D Secure Authentication and Its Importance

3D Secure authentication works to protect online merchants from fraud and chargebacks while making transactions safer for everyone. 3D Secure proves that a transaction’s real cardholder made the purchase by verifying their identity before processing.

3D Secure payments offer several key benefits to both merchants and consumers:

- Reduced Fraud Risk: The main benefit of 3D Secure is its strong protection against unauthorized transactions because it adds an authentication step before payment processing.

- Liability Shift: Through 3D Secure payments, card issuers assume responsibility for transaction verification, and merchants escape liability for chargebacks.

- Enhanced Customer Trust: 3D Secure helps customers feel secure about their financial data since identity verification happens during the authentication process, which protects against fraud and identity theft.

- Stronger Authentication: Customers need to perform additional identity verification through 3D Secure because this service protects online transactions from unauthorized use.

- Global Compliance: Many regions adopted new rules to protect online payments, which led to the implementation of Strong Customer Authentication (SCA) under PSD2 across the European Union.

Read more: Expense management

The Evolution of 3D Secure: From 1.0 to 2.0

The first version of 3D Secure (3D Secure 1.0) created an authentication system that allowed customers to verify their identity by entering passwords or one-time passwords. This security measure added protection but created user inconvenience and raised the chance of canceled transactions.

In 2016, the introduction of 3D Secure 2.0 enhanced the authentication process through merchant data sharing with card issuers across multiple dimensions. The extra details sent to the issuer assist in evaluating transaction risk and making authentication decisions.

Key features of 3D Secure 2.0 include:

- Faster Authentication: 3DS 2.0 allows secure transactions to move faster by eliminating the need for customers to enter a password or OTP until extra verification is needed to help reduce cart abandonment and make checkout faster.

- Better User Experience: 3D Secure 2.0 eradicates the need for redirects and pop-ups. Thus, it makes the authentication process smoother and very less invasive. 3D Secure 2.0 runs the overall security checks automatically in the background to safeguard customers from disruption when they shop online.

- Mobile-Friendly: With the growing use of mobile phones for online purchases, 3D Secure 2.0 was developed to be more mobile-friendly. 3D Secure 2.0 lets customers verify their identity with their device’s built-in security means, such as fingerprint and facial scans.

- Additional Data Sharing: For better fraud detection, the protocol authorizes the merchants and card issuers to exchange complete transaction details like device data, shipping addresses, and purchase history.

- Compliance with PSD2: Online businesses in the EU can continue their normal payment operations with 3D Secure 2.0 because it meets Strong Customer Authentication requirements under PSD2 regulations.

Read more: Account receivable process

How 3D Secure impacts Mobile Payments

The growing use of mobile commerce makes mobile payment security more essential than before. 3D Secure shows its power by making mobile payments safer and solving their special device issues. Mobile customers look for easy and protected shopping on their phone or tablet screens, and 3D secure technology adapts to meet these demands.

3D Secure 2.0 developed a security protocol that optimizes mobile device compatibility. Mobile payments face challenges due to small screens, but 3D Secure 2.0 solves this by offering simple authentication methods that work well on smartphones. For example, the protocol now backs biometric authentication. Users can now authenticate with their body features, such as fingerprints or facial scans, to make the login process faster and more convenient. 3DS payments lessen the chances of unauthorized transactions a great deal, even if someone has hampered with the card details.

Through 3D Secure 2.0, users can now complete payment authentication within their mobile app or website without needing to switch to an external page. The entire 3d secure authentication process happens directly on the mobile app or web page without interrupting the checkout process. Maintaining a smooth customer journey and lowering cart abandonment rates depends heavily on this system.

Some key benefits of 3D Secure 2.0 for mobile payments include:

- Frictionless Authentication: The system lets users shop securely without entering more details for basic transactions. The system performs authentication silently and lets customers proceed with their transactions without delay.

- Mobile-Friendly User Interface: The protocol works better on mobile devices because it adapts to small screens and touch control systems. Users avoid entering passwords and dealing with complex authentication screens during their online activities.

- Biometric Authentication: 3D Secure 2.0 lets users verify their identity through facial or fingerprint scans. Mobile payments become more secure and easier to use when users no longer need to remember passwords.

- Improved Security: When cybercriminals target mobile devices, 3D Secure 2.0 protects consumers and merchants better through real-time risk assessments and strong encryption.

- Better Compliance with Regulations: Under PSD2 regulations in the European Union, mobile payments need to follow Strong Customer Authentication standards, and 3D Secure 2.0 fulfills these requirements.

Read more: Financial accounting

3D Secure Technology Stands as a Key Solution to Stop Online Fraud Attacks

3D Secure (3DS) helps e-commerce businesses fight online fraud by adding secure verification steps to protect both their customers and their money. Before 3D Secure, online payments needed little more than a card number, expiration date, and CVV, yet thieves could still use stolen card data to make unauthorized transactions. 3D Secure adds an identity verification process to payment transactions, making fraudulent transactions far less likely.

3D Secure confirms that the cardholder is making the transaction by checking their identity before processing the purchase. The system requires card owners to verify their identity using SMS or email OTP codes or biometric scans based on the selected 3D Secure implementation.

3D Secure protection shields merchants from financial losses by deterring fraudulent transactions. When a merchant uses 3D Secure, their liability shifts to that of the card issuer because they have implemented the authentication steps to verify the transaction. The protection system helps stores keep their money from fraudulent deals while building customer confidence.

By acting as a strong fence between the fraudsters and the consumers’ personal information, 3D Secure is quite vital in preventing a wide range of deception types. These may include:

- Card-not-present fraud: Thieves mainly use stolen credit card numbers to conduct online transactions without authorization.

- Account takeover: Cybercriminals use stolen login information to make unauthorized transactions through real accounts.

- Chargeback fraud: When someone uses fraudulent chargebacks against a valid purchase to receive free items without paying.

The protocol stops fraudulent transactions by confirming user identity before proceeding with any e-commerce purchases.

Read more: Spend analysis

Conclusion

Thanks to advanced 3D Secure technology, online payments now have better protection than ever before against fraud threats. 3D Secure payments create an added security shield that lowers the chances of fraudulent transactions and chargeback issues. 3D Secure (3DS) plays a pivotal role in mitigating online fraud by adding an extra layer of authentication during the transaction process.

The release of 3D Secure 2.0 made the protocol easier to use on mobile devices and more compliant with global regulations like PSD2 while keeping online shopping secure.

Understanding how 3D Secure affects payment gateways and requires customer authentication helps businesses choose better payment systems while building a safer online shopping experience for their customers.

FAQs

How does 3D Secure 1.0 differ from 3D Secure 2.0?

The latest version of 3D Secure represents an upgraded iteration of the original security protocol. 3D Secure 2.0 provides better transaction security and an easier mobile interface than 3D Secure 1.0. It adds security layers with biometric recognition and lets customers pass through checkout easily while helping companies meet PSD2 rules in Europe.

How does 3D Secure impact the speed at which payments happen and how users feel during their transactions?

Although 3D Secure boosts transaction security, it leads to more steps in the buying process, including one-time passcode and biometric verification. The new version of 3D Secure lets many transactions go through 3d secure authentication without needing user input to reduce the number of steps needed. The system keeps security measures in place while also providing faster transactions.

Explain how the use of 3D Secure is necessary for every online payment, regardless of the transaction type.

3D Secure is legally required in certain regions, particularly in the European Union. The European Union’s PSD2 regulations and Strong Customer Authentication requirements force regional merchants to use 3D Secure. However, the majority of countries let merchants and buyers choose if they want to use 3D Secure. Even if 3D Secure is not mandatory, merchants can use it to fight fraud in their region.

How does 3D Secure work with debit and credit cards from all bank issuers worldwide?

3D Secure works with Visa Mastercard, American Express, and Discover when they participate in the network. Every banking institution sets rules about which cards they enroll in the 3D Secure system. Users must contact their bank to start the 3D Secure registration process for specific credit and debit cards.

How does 3D Secure technology work for all digital wallet payments that link to enrolled credit or debit cards?

You can use 3D Secure when paying with digital wallets, Apple Pay, and Google Pay if your linked payment card participates in the 3D Secure program. Additional security features in digital wallets enhance protection, but they work best when combined with 3D Secure technology.

Does the 3D Secure security system trigger more transaction failures?

The enhanced security of 3D Secure reduces fraud, meaning customers have less risk of chargebacks. Customers might abandon transactions when additional authentication steps prove difficult or confusing to complete. 3D Secure 2.0 seeks to create a smooth authentication process for users.

What actions should business owners take when their customers fail the 3D Secure authentication process?

When payment gets rejected during 3D Secure authentication, merchants need to find out why the payment failed. Payment failure results from either a low bank balance, card restrictions, or issues with the banking system. The merchant should contact their payment gateway provider to fix the purchasing problem for their customers.

What expenses will merchants face when they adopt 3D Secure?

Setting up 3D Secure for payment processing demands an investment in an MPI to link with the payment gateway, payments per transaction, and possible installation expenses. Most payment processors include 3D Secure as part of their basic services, and merchants need to evaluate if fraud protection benefits cover the setup expenses.

What security measures does the 3D Secure provide in subscription payment scenarios?

During the first setup or when customers use a different payment method, 3D Secure validates their subscription-based transactions. After customers verify their identity, they can often make future payments without reauthenticating based on the issuer’s risk assessment.

Does 3D Secure technology work with payment methods beyond traditional cards?

3D Secure works only with card payments because it was built to protect these specific transactions. However, two-factor authentication procedures (2FA) help safeguard transactions that are different from standard card payments.