Unified Payments Interface (UPI) has transformed the way digital transactions work in India, offering a fast, secure, and hassle-free payment experience. Whether you’re new to UPI or looking for more clarity on its features, security, or troubleshooting, you might have several questions.

This blog answers the most frequently asked questions about UPI, covering everything from setting up your UPI ID to handling transaction failures and refunds. No matter which UPI-enabled app or banking platform you use, this guide will help you navigate the system with confidence.

Read on to get all your doubts resolved and make the most of UPI’s seamless payment experience!

What is UPI Payment: A Brief

UPI, or Unified Payments Interface, has revolutionized how India pays. It was officially launched in April 2016 and was developed by NPCI or National Payments Corporation of India. Of course, most people hesitated back then to adopt the idea of going cashless. However, as years passed, people have learned how convenient and safe it is to use UPI as a payment method.

You can transfer funds between bank accounts via smartphones whenever you want. This means that you don’t have to worry if you do not have enough cash in your wallet. Just grab your phone and use the UPI payment app to make the payment. Moreover, the system is designed for ease of use and works 24/7. If your food delivery guy says he doesn’t have a change and no shop is open nearby because it’s 2 am at night, just pay via UPI and enjoy your food. Isn’t UPI an efficient alternative to traditional banking methods?

With UPI, you can make quick payments using a mobile device. It eliminates the need for card details or entering account information. Instead, you use a Virtual Payment Address (VPA). UPI enables secure and hassle-free transfers, even across different banks.

UPI provides features like “Send Money” and “Collect Money.” These allow peer-to-peer (P2P) and peer-to-merchant (P2M) transactions. This means you can pay a person you owe money to, and you can pay a business you purchased something from.

From sending money as a gift to your loved ones to paying electric bills, booking trains, purchasing groceries, and more, UPI works everywhere, every time.

What is VPA in UPI Payment?

A VPA is a unique identifier used in UPI transactions. The VPA replaces traditional account details, making payments simpler and more secure.

You can set your VPA when registering for UPI. It links to your bank account and allows easy transfers. This address does not require sharing your bank account number or IFSC code.

VPAs provide anonymity while making transactions. You can create multiple VPAs for different purposes, such as one for personal use and one for business.

A VPA helps streamline the payment process. It is simple to remember and share. For instance, if you want to send money to a friend, you only need their VPA, not their bank details. Similarly, businesses can use VPAs to accept payments directly into their accounts.

Read More: UPI Payments

Setting Up UPI Payment

Setting up UPI payments is straightforward. Here’s a simple guide to get started:

- Download a UPI-enabled app.

- Register your mobile number. The mobile number used must be linked to your bank account.

- Link your bank account. Choose your bank from the list of UPI-enabled banks. Enter your bank account details in the link.

- Create a UPI ID. This is your VPA, and it can be something simple like yourname@upi.

- Set your UPI PIN. This is a 4-6 digit number that will be required for every transaction.

Once you’ve set up your UPI account, you’re ready to send and receive money. You can make payments online, pay bills, take subscriptions, transfer funds instantly, and more.

How to Make UPI Payment

UPI payments are based on a simple and secure process. Here’s a breakdown of how UPI payment works:

- Step 1: Open your UPI app.

- Step 2: Enter your UPI ID or select the receiver’s VPA.

- Step 3: Choose the amount you want to transfer.

- Step 4: Authenticate using your UPI PIN.

- Step 5: The money is instantly debited from your account and transferred to the receiver’s account.

The entire process takes just a few seconds. UPI uses a two-factor authentication system to ensure security. It works 24/7 and even on holidays.

Read More: Payment Gateway

How to Use Credit Cards for UPI Payments

Using a credit card for UPI payment is simple. First, ensure that your UPI app supports credit card payments. Many UPI-enabled apps now allow linking of credit cards.

Here’s how it should be done:

- First, ensure that your UPI app supports credit card payments. Link your credit card by adding it to the app’s payment settings.

- When making a payment, select UPI as your payment option.

- Choose your linked credit card from the available options.

- Confirm the transaction by entering your UPI PIN for security.

The payment will be instantly processed, and the amount will be debited from your credit card. However, the thing you have to remember is that not all UPI apps or banks support credit card transactions via UPI. So, it’s essential to check before attempting this.

What is the UPI Payment Limit

There are defined transaction limits for UPI payments to ensure security and manage the flow of funds. These limits vary based on the type of transaction and user:

- Standard limits: For normal transactions, the UPI limit is typically Rs. 1 lakh per transaction. However, the total number of transactions allowed is usually up to 20 per day.

- First-time users: New UPI users may face lower limits, generally up to Rs. 5000, in the first 24 hours of their first UPI transaction.

- Category-specific limits: For some specific categories, such as stock market investments, insurance premiums, or foreign inward remittances, the transaction limit may be increased up to Rs. 2 lakh or more.

- Increasing the limit: You can increase your UPI limit by requesting it from your bank, provided you meet their eligibility criteria.

Read More: UPI Transaction Limit Per Day

Increasing UPI Payment Limit

UPI has a default transaction limit, which may vary based on the bank or app. However, increasing your UPI payment limit is possible in certain situations. Here’s how you can raise the limit:

- Contact your bank: Some banks allow users to increase their UPI transaction limits if they make a request.

- Eligibility criteria: Ensure you meet the requirements set by your bank. For example, you may need to verify your identity through KYC (Know Your Customer) processes.

- Check UPI app settings: Some UPI apps also allow you to increase the limit. Look for options under your account settings or payment preferences.

If you’re planning to make high-value transactions, consider checking with your bank for higher limits. Some banks allow up to Rs. 2 lakhs per transaction for certain categories.

How to Reverse UPI Payment

UPI payments are generally instant, but sometimes, issues can arise that require payment reversals or refunds. In cases where a transaction fails or an incorrect payment is made, UPI has mechanisms to handle these situations.

Here’s how payment reversals and refunds work:

- Automatic Reversal: If a UPI payment fails due to a technical error, the system usually initiates an automatic reversal. The funds are returned to your account within a few hours, typically within 24 hours.

- Failed Transaction: In the case of a failed transaction, where money is debited from your account but not received by the recipient, you should wait for a while. Most transactions are reversed automatically by the UPI system.

- Manual Refund: If the transaction doesn’t reverse automatically, contact your bank’s customer support. They can guide you through the process of initiating a manual refund or troubleshooting the issue.

- Dispute Resolution: If the transaction is disputed (such as fraud or unauthorized payment), you can raise a dispute through the UPI app. The bank will investigate and may issue a refund if deemed necessary.

Read More: Payment Links

How to Cancel UPI Payment

Canceling a UPI payment is not as simple as other payment methods. Once a UPI payment is initiated and processed, it generally cannot be canceled. However, there are a few options to explore in case of errors or issues.

If you’re still on the payment screen and haven’t entered your UPI PIN, you can cancel the transaction by navigating away or closing the app. Once the payment has been processed and confirmed by the app, you can’t directly cancel it. UPI doesn’t support a direct stop payment request.

However, if there’s an error, such as paying the wrong person or sending incorrect details, you can request a refund from the recipient. If the funds are not received, check with your bank or the UPI app for assistance. If the transaction is unsuccessful but funds were debited, contact your bank’s customer support. They will guide you through the reversal process.

How UPI is Transforming Merchant Payments

By providing a faster, more secure, and cost-effective alternative to traditional payment methods, UPI has revolutionized merchant transactions.

Here’s how UPI is reshaping merchant payments:

- Instant Payment Processing: UPI enables merchants to receive payments instantly. Unlike traditional methods, where there may be a delay in settlement, UPI ensures real-time transactions, improving cash flow for businesses.

- Cost-Effective: UPI eliminates the need for expensive Point of Sale (POS) terminals or card swipe machines. This reduces overhead costs for small and medium-sized businesses and makes it a more accessible option.

- Easy Integration: UPI offers a simple way for businesses to integrate digital payments. Merchants can easily add UPI payment methods by using QR codes or linking their bank accounts to various payment apps.

- Wider Customer Base: UPI allows businesses to accept payments from a large variety of payment apps. This increases the number of potential customers who can make payments.

- Security: UPI uses encryption and two-factor authentication (2FA), ensuring secure transactions. This builds trust with customers and reduces the risk of fraud.

- Accessibility for Small Merchants: UPI’s low-cost setup makes it ideal for small vendors, street markets, and even remote areas where traditional banking services may not be available.

Read More: Bulk Payment Solution

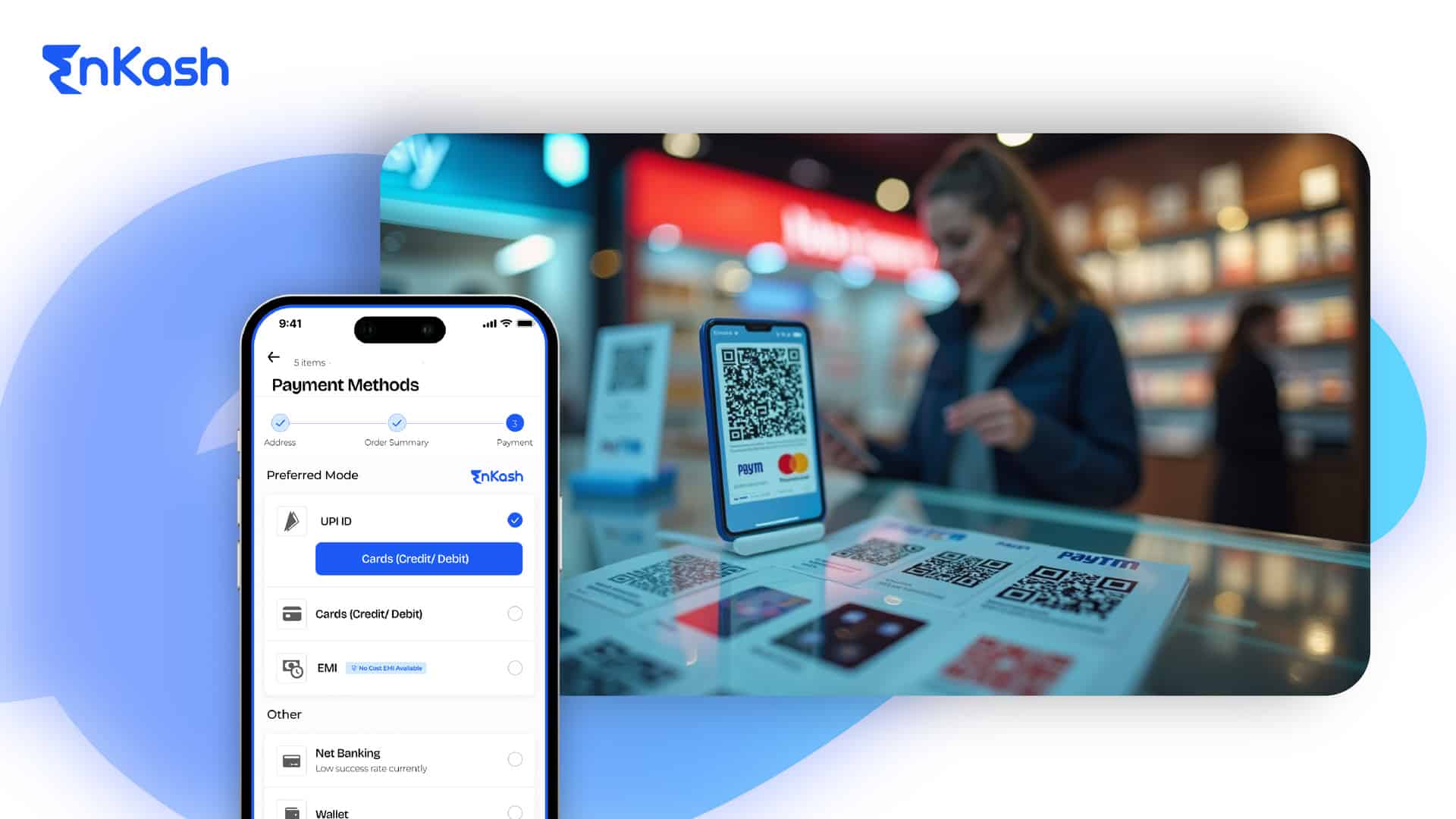

How to Integrate UPI Payment Gateway in Website

Integrating a UPI payment gateway into your website can make it easier for your customers to make secure payments. Here’s how you can do it:

- Choose a payment gateway: Select a reliable payment gateway provider that supports UPI. Popular choices include Paytm, Razorpay, and others. Most gateways provide UPI as a part of their standard payment solution.

- Sign up and set up: After selecting your payment gateway provider, create an account and set up your merchant details. You’ll need to provide business information, bank account details, and other required documents.

- Integrate a payment gateway into the website: Use the integration guide provided by your chosen payment gateway. This usually involves embedding a payment button or link on your checkout page that supports UPI payments.

- Customization options: Many gateways offer customization options, such as adding logos, customizing the payment interface, and providing various payment methods.

- Testing: Before going live, thoroughly test the integration using test transactions to ensure that UPI payments work correctly on your site.

Once integrated, your customers can easily pay using UPI by entering their VPA and completing the payment with a simple authentication step. This increases convenience and trust, enhancing customer experience.

Are UPI Payments Free?

One of the main attractions of UPI is that it is generally free for users. Here’s what you need to know about UPI payment charges:

- No transaction fees: For the majority of UPI users, transactions are free of charge. Whether you’re transferring funds or paying merchants, you won’t be charged extra fees for using UPI.

- Merchant charges: While users don’t typically pay fees, merchants accepting UPI payments might incur small transaction fees. These fees are often absorbed by the merchant or may be included in the pricing of goods and services.

- Bank charges: Some banks may charge small fees for certain services related to UPI, such as setting up or using additional features. Always check your bank’s terms for any hidden charges.

- Third-party apps: Some third-party apps may charge for services beyond standard payments, such as bill payments or wallet loading, but UPI payments themselves remain free.

All in All

UPI has revolutionized the way we make payments, offering a simple, secure, and efficient method to transfer funds across different banks. From peer-to-peer transfers to merchant payments, UPI allows users to complete transactions instantly with just a few taps on their smartphones.

The system’s ease of use, low transaction costs, and robust security features make it a preferred choice for millions of users across India. However, like any payment system, it’s crucial to stay vigilant about security. Always double-check recipient details, safeguard your UPI PIN, and report any issues promptly to ensure your payments are processed securely.

With constant updates and improvements, UPI will continue to evolve, expanding its reach and functionality and helping India move towards a more digital and cashless economy.

FAQs

Can UPI payments be reversed?

UPI payments can be reversed in case of transaction failures. The funds are generally refunded automatically within 24-48 hours. If the funds are not reversed, contact your bank for assistance.

How to increase the UPI payment limit?

To increase your UPI transaction limit, you can contact your bank. Some banks may allow you to raise the limit through their app or customer support.

How to make offline UPI payments?

UPI payments are mostly known for online transactions, but they can also be used offline. The National Payments Corporation of India (NPCI) offers a USSD-based UPI service for users without internet access. You can dial *99# from your mobile and follow the prompts to make UPI payments

What happens if I forget my UPI PIN?

If you forget your UPI PIN, you can reset it using your linked debit card details (last six digits and expiry date) through your UPI app. An OTP will also be required for verification.

Can I use UPI without a bank account?

No, UPI requires a bank account linked to your mobile number. However, you can also link Prepaid Payment Instruments (PPIs) or wallets to UPIs for making payments, as long as they are supported by your UPI-enabled app.

Is it possible to link multiple bank accounts to a single VPA?

You can link multiple bank accounts to the same Virtual Payment Address (VPA). This allows you to choose from any of your linked accounts while making UPI payments.

How can I cancel a UPI payment?

Once a UPI payment is processed and confirmed, it cannot be canceled. However, if the transaction fails, the payment is typically refunded within 24-48 hours. You can contact your bank for support if needed.

How to block a UPI payment?

If you suspect fraud or unauthorized activity, you can contact your bank immediately to block the UPI service for your account. They may help suspend payments temporarily while investigating the issue.

Can I make payments through UPI using a credit card?

Yes, many UPI apps now allow linking a credit card to make payments. You can select the credit card as a payment option while completing a UPI transaction and authenticate using your UPI PIN.

How to check if a UPI payment has been credited?

You can check the status of a UPI payment through the “Transaction History” section of your UPI app or by reviewing your bank statement. You might also receive an SMS or push notification confirming the payment status.

What is the maximum amount I can transfer using UPI?

The standard UPI transaction limit is Rs. 1 lakh per transaction. However, limits may vary based on your bank and transaction category, such as for investments or insurance payments.

Can I use UPI for international payments?

No, UPI is currently designed for domestic transactions within India. You cannot use UPI to send money abroad or make payments in foreign currencies. However, some countries like Nepal, France, and more have partnered with UPI. You can use UPI payments in these particular countries.

How to integrate a UPI payment gateway into my website?

To integrate a UPI payment gateway into your website, choose a payment provider that supports UPI. Follow the provider’s integration guide to embed UPI as a payment option during checkout.

Can UPI payments be made using a virtual card or wallet?

Yes, some UPI apps allow you to link virtual cards or PPIs like mobile wallets for making payments, provided the app supports this feature.

How do I reset my UPI PIN on a new device?

If you switch to a new device, you can reset your UPI PIN by verifying your phone number and debit card details. You will receive an OTP to authenticate the process on your new device.

Can I link my NRE or NRO account with UPI?

Yes. Even if you are an NRI, you can link both NRE and NRO accounts to UPI, provided your registered mobile number is from an Indian service provider.

What should I do if my UPI transaction is showing as “pending”?

If your UPI transaction is marked as pending, wait for 24-48 hours, as it could be due to network or banking issues. If it remains pending, contact your bank for assistance or to inquire about the status.

How can I link a second bank account to my UPI ID?

To link a second bank account to your UPI ID, open your UPI app. Go to account settings and select “Add Account.” Choose your bank and verify with your UPI PIN. Your second account will then be linked. You can switch between linked accounts when making payments.

Is there a transaction fee for UPI payments?

For most users, UPI transactions are free. However, some third-party apps or banks might charge fees for specific services, like platform charges and more.

Can I use UPI to pay utility bills?

Yes, UPI can be used to pay utility bills such as electricity, water, and broadband bills. Most service providers support UPI as a payment method, and you can make payments directly from your UPI-enabled app.

What should I do if my UPI payment is debited but the recipient didn’t receive it?

If the money was debited from your account but the recipient hasn’t received it, wait for up to 48 hours for the transaction to be processed. If the issue persists, contact your bank to raise a dispute or request a reversal.

Can I link a business account to UPI?

Yes, you can link a business account to UPI. Merchants or businesses can set up UPI payment gateways and create unique VPA for receiving payments directly into their business accounts.

Can I use UPI to pay at restaurants or shops?

UPI is commonly used for in-store payments. You can either scan the merchant’s QR code or provide your VPA to the merchant to complete the payment instantly, making it a convenient option for transactions.

How can I report fraud or unauthorized UPI transactions?

If you suspect fraud or an unauthorized transaction, contact your bank immediately. You can also raise a complaint through the UPI app or your bank’s customer support service to block your account and investigate the issue. It is also important to file a complaint with the National Cyber Crime Reporting Portal, or you may dial 1930.

How can I update my UPI ID?

To update your UPI ID, you need to go to your UPI app settings and select the option to change your VPA. Once updated, use your new ID for all future transactions.

Can I transfer money from UPI to my bank account?

No, you cannot transfer money directly from UPI to your bank account. UPI is designed for transferring money between bank accounts. However, if you receive money via UPI, it will be credited to your linked bank account automatically. You can withdraw the amount from your bank account using other methods such as an ATM, over-the-counter transactions at the bank, etc.

Can I link my UPI ID to multiple mobile numbers?

No, a UPI ID can only be linked to one mobile number. However, you can link multiple bank accounts to the same UPI ID.

Can I use UPI for peer-to-peer lending or borrowing?

UPI is primarily for payments. However, it can be used for peer-to-peer lending or borrowing if both parties agree on the terms and use UPI for transferring funds.

Is there a way that will enable me to secure my UPI account from fraud?

First and foremost, enable two-factor authentication. Set a strong UPI PIN and strictly avoid sharing that and your account details. Use only trusted UPI apps. Additionally, transaction history should be monitored regularly. If you notice any kind of suspicious activity, report it as soon as possible.

Is there any maximum daily limit set for UPI transactions?

Yes, there is. The daily limit for UPI transactions is typically Rs. 1 lakh. However, this may vary by bank and depending on the user profile. Some banks even let users transact up to Rs. 2 lakh or more. But they belong to specific transaction categories.

What is the UPI mandate, and how is it used?

A UPI mandate is an authorization that allows recurring payments to be automatically debited from your account. It’s used for services like subscription renewals or utility bill payments. You can set up mandates within UPI-enabled apps.

How do I withdraw money from my UPI wallet?

To withdraw money from your UPI wallet, open your UPI-enabled app. Navigate to the “Balance” or “Wallet” section. Select the option to transfer funds to your linked bank account. Enter the amount you wish to withdraw. Confirm the transaction by entering your UPI PIN. The money will be transferred instantly to your bank account. Make sure your UPI wallet has enough balance for the transaction.

How can I disable or deactivate my UPI account?

There might be various reasons behind a user wanting to deactivate their UPI account. To do that, you must open your UPI app. Navigate to the “Settings” or “Profile” section. Look for the option to “View Profile” and select it. You will find the “De-register” option there. Click on it to deactivate your UPI account. Once deactivated, your UPI ID cannot be used again. For further assistance, contact your bank’s customer support.

Can I receive UPI payments from someone who is not registered on UPI?

Yes, you can receive payments via UPI even if the sender is not registered on UPI, provided they send money using their bank details (like Account Number + IFSC or mobile number) instead of a VPA.