Most of India’s population today uses e-payments to settle their dues, even the very minor ones. From serious payments like insurance premiums, business transfers, etc., to daily exchanges like grocery shopping, cab booking, and more, people use digital payment methods almost everywhere. However, not all of them might be familiar with the term “Payment Gateways” or “e-Payment Gateways.” It might just be UPI or a digital wallet for them that they are opening to pay at a petrol pump, or being redirected to when shopping online. But there is a lot more behind the umbrella term “e-Payment Gateways” that makes every digital payment accurate, fast, and secure.

Before getting into details, it is important to note that payment gateways and e-payment gateways are synonymous. They refer to the same technology.

So, to define an e-payment gateway, we can say that it is a service that facilitates secure online money transactions between customers and merchants. You can think of it as a bridge between these two parties. This bridge-like payment gateway lets both of them exchange funds over the internet securely.

The term “security” is important here, as online fraud is a huge concern for everyone. Both merchants and customers want the transactions to be secure without leaking any bank-related details that could attract online fraudsters. And e-payment gateways ensure that. Otherwise, they wouldn’t have gained so much popularity over time and become the most popular way of handling payments, would they?

So, the payment gateway meaning indicates nothing but a secure digital tool that handles online payments. Without it, completing online purchases securely would be nearly impossible.

Understanding E-Payment Gateway

To get into a bit more detail, an e-payment gateway operates by encrypting the payment information. This ensures that the data is securely transmitted from the customer to the merchant’s bank or payment processor. Once the payment data is sent, the gateway works with the payment processor. The processor validates the transaction and checks for any fraud. It then approves or declines the payment based on the information. If the transaction is approved, the gateway sends the approval back to the merchant. This completes the transaction and confirms that the payment was successful.

This happens so quickly that it is hard to believe all these processes that are going on in an e-payment gateway. Payments reach the merchant’s bank in just seconds, and both parties get notifications about that.

Key Functions of E-Payment Gateways

- Authorization: Verifying if the customer has sufficient funds or credit.

- Encryption: Securing transaction data through encryption protocols, like SSL.

- Fraud Protection: Using AI and algorithms to detect and prevent fraud.

- Settlement: Ensuring that funds are transferred from the customer to the merchant’s account.

- Compliance: Adhering to security standards, such as PCI-DSS, to protect customer data.

The Evolution of E-Payment Gateways

Over the years, key developments have made online payments faster, safer, and more accessible. Here’s a detailed look at e-payment gateways’ evolution:

Early Days – Manual Payment Processing

In the early days of e-commerce, payments were not automated. Customers had to rely on traditional methods, like phone calls and fax orders, to complete transactions. Businesses manually processed these payments, which led to delays and errors. There were no secure digital solutions to verify transactions or protect sensitive data. Manual payment processing was time-consuming and prone to mistakes.

First Generation – Basic Online Transactions

The first e-payment gateways appeared in the late 1990s. They allowed businesses to accept credit card payments online. However, security was limited. These gateways lacked encryption, which made them vulnerable to fraud. Transactions were processed in batches, which meant customers had to wait for confirmation. The technology was new and basic, enabling only simple payments without real-time processing or robust fraud protection.

Second Generation – Secure Online Payments

As e-commerce grew, the need for secure and fast transactions became clear. In the early 2000s, SSL encryption became standard for securing payment data. This encryption ensured that sensitive customer information, such as credit card details, was protected. Fraud protection systems were also integrated into payment gateways, reducing the risk of unauthorized transactions. With these enhancements, real-time payment processing emerged, offering faster transaction approvals and instant confirmation for customers and merchants.

Third Generation – Mobile and Alternative Payments

As smartphones became mainstream in the late 2000s, mobile payments took off. E-payment gateways began to support mobile wallets like PayPal, Apple Pay, and Google Pay, making payments even more convenient. QR codes became popular for easy in-person transactions. Additionally, alternative payment methods like UPI or Unified Payments Interface were introduced in countries like India, enabling customers to make direct bank transfers using their mobile phones. These developments significantly expanded the range of payment options available to consumers, improving user experience and making online shopping more accessible.

Current Generation – AI and Automation

Today, e-payment gateways are more sophisticated than ever. With the rise of Artificial Intelligence (AI) and machine learning, gateways are now able to detect fraud more efficiently. These technologies analyze vast amounts of transaction data in real time, spotting potential risks and preventing fraudulent activities. Tokenization has replaced sensitive payment data with secure randomized tokens, ensuring that personal information is never exposed. Additionally, blockchain technology is being explored to enhance transaction transparency and reduce the risk of fraud. This era focuses on security, speed, and automation to create a seamless payment experience for consumers and merchants.

How Payment Gateways Work: Step-by-Step Process

We have already discussed how e-payment gateways work in brief. Let’s understand it with more particular details in this section.

Knowing how a payment gateway works is crucial for anyone involved in online transactions. The payment gateway process involves several key steps, each ensuring a secure and successful payment. Here’s how it happens:

- Customer Initiates Payment:

- The customer selects a product or service.

- At checkout, they enter payment details, such as credit card information, UPI ID, or e-wallet credentials.

- This action triggers the e-payment gateway.

- Data Encryption & Transfer:

- The payment gateway encrypts sensitive payment information.

- Encryption ensures that data like card numbers are secure.

- The encrypted data is then sent to the payment processor or bank.

- Routing to Processor/Bank:

- The payment gateway forwards the data to the merchant’s acquiring bank.

- This data is then routed to the relevant card network (Visa, MasterCard) or payment network.

- The processor checks if the payment method is valid.

- Authorization by Issuing Bank:

- The customer’s bank (issuing bank) verifies the transaction details.

- The bank checks if there are sufficient funds or credit.

- It also performs fraud checks and may request two-factor authentication (e.g., OTP).

- Response Relayed to Merchant:

- The issuing bank either approves or declines the payment.

- This response is sent back through the payment network and processor to the e-payment gateway.

- The gateway then sends the approval or decline message to the merchant’s site.

- Funds Settlement:

- If approved, the funds are transferred from the customer’s bank to the merchant’s bank.

- This happens through the card network or payment processor.

- The settlement may take up to 1–2 business days, depending on the gateway.

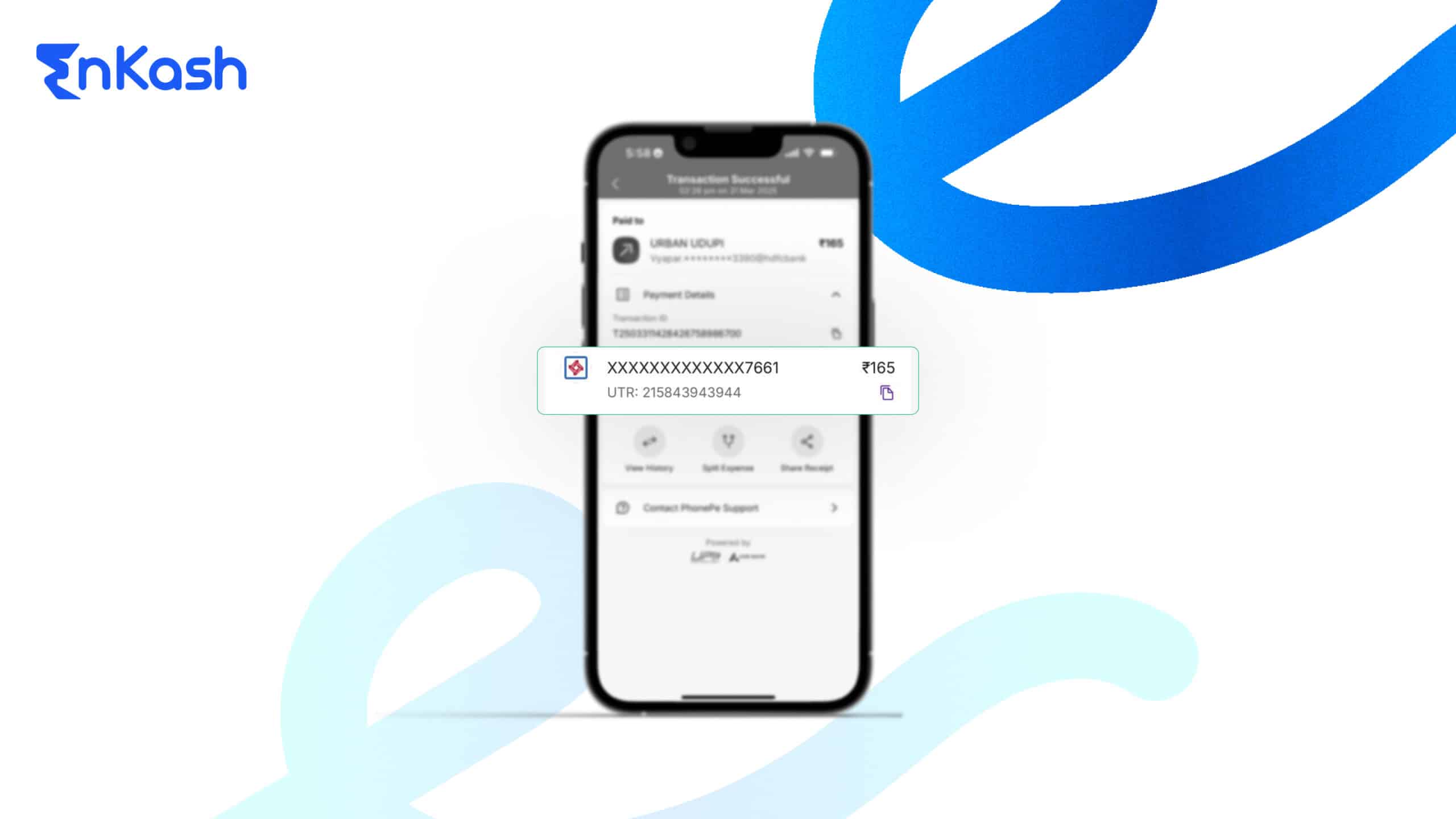

- Confirmation & Receipts:

- The merchant confirms the transaction and provides the customer with a receipt.

- The payment gateway may also send an email or SMS notification to the customer for confirmation.

As mentioned before, this entire process occurs in seconds, providing a seamless and secure transaction for both the customer and the merchant.

Types of Payment Gateways

E-payment gateways come in different types, each suited to various business needs and integration preferences. Let’s explore the different types and how they function:

1. Hosted Payment Gateways (Redirect Method)

In a hosted payment gateway, the customer is redirected to the payment service provider’s (PSP) page. After the customer enters their payment details, they are redirected back to the merchant’s site. Some common examples are PayPal, Razorpay, and CCAvenue.

Pros:

- Easy setup for merchants.

- The payment service provider handles security and compliance (like PCI-DSS).

Cons:

- Adds an extra step in the checkout process.

- The merchant has less control over the user interface.

2. Self-Hosted/API Integration Gateways

In this setup, customers enter payment details on the merchant’s site itself. The payment information is then securely passed to the e-payment gateway via an API (Application Programming Interface). Examples include Stripe, PayU, and Razorpay API integration.

Pros:

- Provides a seamless checkout experience.

- Full control over the user interface and branding.

Cons:

- Requires technical expertise for integration.

- The merchant must ensure security compliance (PCI-DSS).

3. Bank Payment Gateways

Bank payment gateways are provided directly by a bank. The merchant integrates the gateway provided by the bank they work with. Examples include HDFC’s PayZapp, ICICI’s Payseal, etc.

Pros:

- Reliable since it is backed by the bank.

- Often cheaper for merchants already banking with the bank.

Cons:

- Limited in payment method options (typically only cards and net banking).

- Less customizable than third-party gateways.

Payment Aggregators vs. Direct Merchant Gateways

Payment Aggregators (like Razorpay, Paytm, or CCAvenue) pool multiple merchants under a single merchant account.

Pros of Aggregators:

- Quick onboarding for merchants.

- Simplifies payment collection for small businesses.

Cons of Aggregators:

- Less control over funds.

- Transaction limits may apply for smaller merchants.

On the other hand, Direct Merchant Gateways require a merchant to have their merchant account with the acquiring bank. Although this gives merchants more control over their payments, it involves a more complex setup process.

Pros of Merchant Payment Gateways:

- Full control over payments and funds.

- Ideal for large businesses with high transaction volumes.

Cons of Merchant Payment Gateways:

- Requires a dedicated merchant account.

- More complex setup and higher costs for small merchants.

Key Components of the E Payment Gateway Ecosystem

The e-payment gateway ecosystem consists of various components and participants that work together to ensure a smooth and secure payment process. Each participant has a specific role, and their interaction is essential for completing online transactions.

Let’s break down these components:

1. Customer (Cardholder)

- The customer initiates the transaction by purchasing a product or service.

- They enter payment details such as credit card information, bank account details, or UPI ID.

- The customer’s role is to authorize the payment by providing the necessary information.

2. Merchant

- The merchant is the business or service provider receiving the payment.

- The merchant sets up the payment gateway on their website or app.

- They use the gateway to securely process payments and receive funds from customers.

3. Payment Gateway

- The e-payment gateway is the technology that captures the customer’s payment data and securely transmits it to the relevant bank or processor.

- It encrypts sensitive information and handles communication between the merchant and the financial institutions involved.

- The gateway often includes additional features like fraud protection and real-time transaction monitoring.

4. Acquiring Bank (Acquirer)

- The acquiring bank is the merchant’s bank that facilitates the acceptance of payments.

- It receives transaction details from the e-payment gateway and sends them to the relevant card network or payment processor.

- The acquirer works to ensure the merchant’s account is credited with the payment amount after a successful transaction authorization.

5. Issuing Bank (Issuer)

- The issuing bank is the customer’s bank that issued the credit card, debit card, or other payment method.

- It verifies the customer’s details, checks for available funds or credit, and approves or declines the transaction.

- The issuer is responsible for ensuring the security and legitimacy of the payment made by the customer.

6. Card Networks / Payment Networks

- Card networks like Visa, MasterCard, or RuPay act as intermediaries between the acquiring and issuing banks.

- They ensure that payment requests are routed through the correct channels and that all transaction data is properly processed and authorized.

7. Payment Processor

- The payment processor is the entity that facilitates communication between the e-payment gateway and the financial institutions (banks, card networks).

- It processes the transaction request and coordinates with the acquiring and issuing banks to approve or decline the payment.

- Payment processors are essential for ensuring that funds are transferred accurately and promptly.

8. Fraud Detection Services

- Fraud detection services play a crucial role in monitoring and preventing fraudulent transactions.

- They use machine learning, data analysis, and rules-based filters to detect suspicious activity.

- These services help minimize chargebacks and protect both merchants and customers from fraud.

9. Regulatory Authorities

- Regulatory authorities, such as the RBI (Reserve Bank of India), ensure that payment gateways operate within legal and security frameworks.

- They enforce standards like PCI-DSS for payment security and monitor compliance with anti-money laundering (AML) laws.

- These authorities protect consumer rights and maintain the integrity of the payment ecosystem.

Read More: Payment Gateway vs Payment Processor

Technical Aspects and Security

E-payment gateways rely on several technical mechanisms to ensure secure transactions. These measures protect both the merchant and the customer. Let’s break down some of the key technical aspects:

1. Encryption

Encryption ensures that payment data is secure. It scrambles sensitive data so only authorized parties can read it.

Payment gateways use SSL/TLS encryption to protect data during transmission. This ensures that details like card numbers remain confidential.

2. Tokenization

Tokenization replaces sensitive card data with random numbers or tokens. The gateway stores the token and not the actual card data. This reduces the risk of data breaches and fraud.

Tokens are used for subsequent transactions, ensuring security.

3. API Integration

Gateways provide APIs to integrate payment processing into merchant websites. APIs allow real-time communication between the gateway and the merchant’s website. Merchants use these APIs to send transaction data to the gateway.

4. 3D Secure (Two-Factor Authentication)

3D Secure requires customers to enter an OTP or password during the transaction. The authentication step ensures that the person making the payment is the cardholder. This reduces fraud for online transactions.

5. PCI-DSS Compliance

The PCI-DSS standard ensures that merchants and gateways protect cardholder data. This compliance requires specific security measures like firewalls and encryption. Merchants who handle card data must follow these guidelines to avoid breaches.

6. Fraud Detection Systems

Fraud detection tools help identify and prevent suspicious transactions. These tools use machine learning to analyze patterns in real time. If a transaction appears risky, the system flags it for further review. Fraud detection minimizes chargebacks and protects customers.

7. Secure Data Storage

Payment gateways do not store card information after a transaction. Sensitive data is either tokenized or encrypted and securely stored. This minimizes the risk of data theft if a breach occurs.

These technical aspects ensure that e-payment gateways function securely and efficiently. They protect sensitive data, prevent fraud, and guarantee safe transactions for both customers and merchants.

Use Cases Across Industries

Payment gateways are essential for many industries, enabling secure, seamless transactions. They are used to process payments across various sectors. Here are some of the key industries and their use cases:

1. E-commerce Retail

E-commerce websites integrate e-payment gateways to accept online payments. Customers can pay using credit/debit cards, wallets, and UPI. Payment gateways help process a large volume of transactions quickly. They ensure secure transactions, preventing fraud during online shopping.

2. Services and Bills

Payment gateways are widely used for paying utility bills, mobile recharges, and insurance premiums. Customers can pay quickly through various methods, including net banking and mobile wallets.

3. Education

Educational institutions use e-payment gateways for fee collections. Students can pay their tuition fees online through a secure gateway. Some gateways also handle payments for online courses and certifications.

4. Travel and Ticketing

Travel agencies, airlines, and ticketing apps integrate payment gateways for booking and ticket purchases. Payment gateways support international and domestic payments through various methods. Features like multi-currency support allow global transactions, making international travel bookings easier. Gateways also handle payments for hotels, buses, and other travel services.

5. Subscription Services

Subscription-based businesses use e-payment gateways for recurring billing. Services like Netflix, Spotify, and gym memberships rely on gateways to charge users periodically. These gateways handle automatic renewals and payment retries for failed transactions. They also manage customers’ payment information securely through tokenization.

6. Donations and Non-Profits

Non-profit organizations use payment gateways to accept donations online. Gateways help facilitate micro-donations, enabling easy contributions through debit cards or UPI. They also provide features like recurring donations, making it easy for donors to contribute regularly.

7. Brick-and-Mortar Retail (Omnichannel Payments)

Physical stores are now using payment gateways to accept online payments via QR codes or payment links. These solutions help merchants manage both in-store and online transactions from a single platform. Omnichannel gateways allow businesses to provide a smooth payment experience across multiple touchpoints.

8. Marketplaces

Online marketplaces like Amazon, Flipkart and food delivery apps use e-payment gateways to facilitate payments. These platforms collect payments from customers and disburse them to multiple sellers. Gateways handle split payments, ensuring each seller gets their share after deducting fees.

These industries rely on payment gateways to offer fast, secure, and flexible payment options. Whether it’s an online store, service provider, or educational institution, payment gateways are integral to smooth transactions.

Compliance and Regulatory Overview

E-payment gateways operate in a structured regulatory environment. Regulations ensure that online transactions are secure, reliable, and transparent.

In India, the Reserve Bank of India or RBI plays a major role in overseeing the payment gateway ecosystem. Let’s explore the main compliance and regulatory aspects that affect payment gateways.

1. RBI Guidelines for Payment Aggregators and Gateways

The RBI issued detailed guidelines for payment aggregators (PAs) and e-payment gateway (PGs). These guidelines regulate their functioning and ensure consumer protection.

- Non-bank payment aggregators must obtain an RBI license to operate. This applies to third-party providers like Razorpay, PayU, and Cashfree, as they handle customer funds, even if briefly.

- Payment gateways like Stripe and CCAvenue, which only route transaction data without handling funds, do not need a license under these guidelines.

- Regulations ensure that these entities maintain a minimum capital requirement (₹15 crore, increasing to ₹25 crore). They are also subject to strict governance and audit practices.

2. Know Your Customer (KYC) and Merchant Onboarding

KYC ensures that only legitimate businesses can onboard with payment gateways.

- Payment gateways must conduct background checks on merchants. This helps ensure they are not involved in fraudulent or illegal activities.

- This process is crucial to prevent crimes such as money laundering, terrorism financing, and other financial crimes.

- The RBI mandates that payment aggregators and gateways establish a merchant onboarding policy that includes KYC checks. This safeguards against scams and illegal operations.

3. PCI-DSS Compliance

Payment Card Industry Data Security Standard (PCI-DSS) is a global standard for handling cardholder data.

- Payment gateways must comply with PCI-DSS requirements to ensure that sensitive card data is securely processed, transmitted, and stored.

- Compliance involves implementing security measures such as encryption, tokenization, and access control. These measures help protect cardholder information from breaches and fraud.

- Failure to comply with PCI-DSS can result in hefty fines and damage to trust among customers.

4. Two-factor authentication

Two-factor authentication (or AFA) is now mandatory for any online transactions you make.

- AFA, or Two-factor authentication, adds an extra layer of security, especially for those transactions where you do not use cards.

- The most common way to implement AFA presently is through 3D Secure protocols.

- Customers must enter an OTP or password during the transaction process.

- In 2023, the RBI mandated AFA even for international card transactions made on Indian merchant websites.

5. Card Tokenization and Data Security

The merchants that store your card details must use tokenization. It has been mandated by the RBI.

- Card information cannot be stored in raw format. It must be replaced with a token, a random identifier representing the card. This protects against card data breaches.

- Payment gateways must comply with these tokenization rules and integrate the system to process transactions securely.

6. Anti-Money Laundering (AML) and Reporting

This one is for e-payment gateways and aggregators. These laws require them to monitor and report suspicious transactions.

- AML has a major role in preventing illegal activities like money laundering and more that might take place during online transactions.

- Gateways must conduct due diligence on high-risk merchants.

- They must also report any suspicious activities they notice through Suspicious Transaction Reports (STR).

7. Data Localization

These laws require all payment data related to Indian transactions to be stored within India.

- As this law is present, regulators can easily access data for investigation and audit purposes.

- Even international payment gateways like Stripe, PayPal, etc., had to comply with this. They specifically set up their data centers in India to store payment data and avoid any foreign exposure.

8. Customer Protection and Grievances

Payment gateways must offer formal mechanisms for resolving customer grievances.

- If a customer faces issues such as payment failures or unauthorized transactions, they can file complaints with the gateway.

- The RBI mandates that payment gateways must have dedicated support channels. They must also issue refunds for failed transactions within a specified time frame (usually T+1 or T+5 days).

9. Transparency in Fees

Payment gateways must disclose any charges related to transactions.

- This includes transaction fees and service charges. Transparent pricing helps both businesses and customers understand the costs involved in using digital payment services.

- The Merchant Discount Rate (MDR), which is the fee charged to merchants for processing payments, must be clearly communicated to customers.

These compliance and regulatory measures ensure that payment gateways operate securely and ethically. The RBI’s guidelines are designed to protect consumers, maintain the integrity of the financial ecosystem, and foster trust in digital payments.

Challenges in the E-Payment Gateway Ecosystem

While e-payment gateways have transformed the way we handle digital payments, the ecosystem faces several challenges. These challenges range from technical issues to regulatory changes, and they impact both merchants and customers. Here are some of the key obstacles:

Transaction Failures and Success Rates

One of the most significant challenges for payment gateways is ensuring a high success rate for transactions. Transaction failures can occur due to reasons like network connectivity issues, bank server downtimes, or incorrect customer details. If a payment gateway experiences frequent failures, merchants may lose customers, resulting in cart abandonment and revenue loss. Payment gateways use techniques like intelligent routing (where the transaction is sent through another acquiring bank if one fails) to mitigate these issues.

Security Threats and Fraud

Online payment systems are always at risk of fraud, making security a primary concern. Cybercriminals attempt to steal card details, conduct phishing attacks, or exploit vulnerabilities in payment systems. Payment gateways must constantly evolve their security measures to combat fraud, using technologies like fraud detection systems, encryption, and tokenization. A major data breach can lead to a loss of customer trust, reputational damage, and legal consequences for businesses.

Integration and Technical Complexity

Payment gateway integration into a merchant’s website or app can be a complex process. For businesses that don’t have in-house technical expertise, integrating a gateway can require custom coding, testing, and troubleshooting. Merchants need to ensure their systems are secure and compliant with PCI-DSS standards, adding to the complexity. Ongoing updates to gateway APIs or new regulations may require merchants to update their systems regularly.

User Experience vs. Security Trade-Off

Security measures like OTP (One-Time Password) verification and two-factor authentication can make the transaction process more secure. However, these additional steps can frustrate customers and lead to a higher cart abandonment rate. Gateways and merchants face the challenge of striking a balance between offering a smooth user experience and ensuring the highest levels of security. Too many security checks might result in a poor customer experience, while minimal security can lead to fraud.

Cost and MDR Issues

MDR (Merchant Discount Rate) is the fee that merchants pay for processing each transaction. High MDR can reduce a merchant’s profitability, especially for businesses with thin margins. The government’s push for zero-MDR on certain payment methods, such as UPI and RuPay debit cards, has reduced costs for merchants but created financial sustainability challenges for e-payment gateways. Gateways need to find alternative revenue streams or optimize transaction volumes to stay profitable, especially when small transactions (like UPI payments) yield low margins.

Regulatory Changes and Compliance Burden

The regulatory environment for e-payment gateways is constantly evolving. New regulations, such as card tokenization or two-factor authentication (AFA) mandates, require payment gateways and merchants to adapt quickly. These compliance changes can be costly and time-consuming for both merchants and payment service providers. Smaller merchants may struggle to keep up with the regulatory overhead, making it difficult to maintain compliance while managing daily operations.

Chargebacks and Disputes

Chargebacks occur when a customer disputes a transaction, and the merchant is forced to return the funds. E-payment gateways help merchants manage chargeback cases, but these can be costly and damaging to a business’s reputation. High chargeback rates may even lead to merchants being blacklisted by acquiring banks or payment processors. Gateways must provide tools to help merchants track disputes, submit evidence, and resolve chargebacks quickly.

Scalability and Downtime

Scalability is crucial for payment gateways, especially during periods of high transaction volume, such as sales seasons or festivals. If a payment gateway faces downtime during peak hours, it can lead to losses in revenue and frustrated customers. E-payment gateways invest in cloud infrastructure and data redundancy to ensure high availability during periods of peak traffic. However, unexpected spikes in demand or system failures can still lead to outages, affecting customer trust.

Customer Trust and Fraudulent Merchants

Customers need to trust that their payment details are handled securely by payment gateways. Phishing scams and fraudulent websites still pose a risk to customers, especially if they fall for fake payment portals. Payment gateways also need to ensure that only legitimate merchants are onboarded onto their platforms. Scammers using an e-payment gateway to conduct fraudulent transactions can damage the gateway’s reputation. Rigorous merchant vetting processes and fraud prevention tools are necessary to maintain trust.

Despite these challenges, the payment gateway ecosystem continues to evolve, with providers constantly innovating to overcome obstacles. Security advancements, better integration tools, and improved user experiences are helping businesses navigate the evolving digital payment landscape.

Conclusion

E-payment gateways have revolutionized the way businesses and consumers handle transactions. These systems enable seamless, secure, and fast payments across a variety of platforms, making them an integral part of the digital economy. As discussed, payment gateways offer solutions for a wide range of industries, including e-commerce, education, travel, and subscription management services.

The evolution of these gateways is driven by several factors, including the increasing demand for secure transactions, the integration of advanced technologies like AI, biometrics, and blockchain, and the regulatory frameworks that ensure safety and compliance. As digital payments become more ubiquitous, we will continue to see innovations that further simplify and secure the payment process.

The future of payment gateways is bright, with innovations continually emerging to meet the needs of both merchants and customers. As businesses and consumers alike embrace these new technologies, payment gateways will continue to be at the core of the digital payment ecosystem, driving growth and evolution in the years to come.

FAQs

What is the difference between a payment gateway and a payment processor?

An e-payment gateway acts as a digital middleman. It securely transmits payment information from the customer to the merchant’s bank. It encrypts the transaction data to ensure security. A payment processor handles the actual transaction. It communicates with the card networks and issuing bank to authorize and transfer funds. The processor makes sure that the funds are debited from the customer’s account and credited to the merchant’s account.

Can I use a payment gateway for recurring billing?

Yes, you can. Many e-payment gateways like Razorpay and Stripe offer recurring billing services. This allows merchants to automatically charge customers on a set schedule, such as weekly, monthly, or annually. Recurring billing is ideal for subscription-based services like streaming platforms or membership sites. The system securely stores customer payment details and processes payments on specified dates, minimizing manual intervention.

How do I choose the right e-payment gateway for my business?

Start by evaluating fees, including setup fees and transaction fees. Next, ensure that the gateway supports the payment methods you need, such as credit cards, UPI, or wallets. Look for easy integration with your website or app, and check for security features, like PCI-DSS compliance. Customer support and a good success rate are crucial. Choose a gateway that is scalable for future growth.

Is it safe to store credit card details with an e-payment gateway?

Storing credit card details directly on your website or app is risky. Instead, use an e-payment gateway that complies with PCI-DSS standards and employs tokenization. Tokenization replaces card information with randomized tokens, making it useless to hackers. Payment gateways never store raw credit card data. They store tokens instead, reducing the risk of sensitive information being compromised.

What types of payments can be processed through a payment gateway?

Payment gateways can process various payment methods, including:

- Credit/debit cards (Visa, MasterCard, American Express)

- UPI (Unified Payments Interface)

- Wallets

- Net banking (from major banks)

- EMI (Equated Monthly Installment) options

- Buy Now Pay Later (BNPL) services

This flexibility allows businesses to serve a broad range of customers.

Can I integrate a payment gateway with my mobile app?

Yes, most modern payment gateways offer easy integration with mobile apps. They provide SDKs (Software Development Kits) and APIs to help developers implement payment processing within the app. Popular gateways like Razorpay and Stripe offer seamless integration, allowing customers to make secure payments directly within the app.

Can a payment gateway support international transactions?

Yes, many payment gateways support international transactions. They allow businesses to accept payments in multiple currencies. Some gateways, like PayPal and Stripe, also handle currency conversion. International transactions are processed with additional security measures and may have higher fees due to the involvement of multiple banks and payment networks.

What is the Merchant Discount Rate (MDR)?

The Merchant Discount Rate (MDR) is the fee charged to the merchant by the e-payment gateway for processing a payment. The fee is typically a percentage of the transaction amount and may vary based on the payment method (card, UPI, wallet). The MDR covers processing costs and security measures, but businesses should compare MDRs from different gateways to minimize transaction costs.

How do payment gateways handle chargebacks?

A chargeback occurs when a customer disputes a payment. The payment gateway notifies the merchant and may reverse the payment if the dispute is valid. Gateways usually provide tools to help merchants handle chargebacks, including submitting evidence of the transaction. A high number of chargebacks can lead to penalties or account termination for the merchant. Payment gateways often help by offering chargeback prevention tools like fraud detection and customer verification.

What is the role of the acquiring bank in payment gateway transactions?

The acquiring bank is the merchant’s bank. It provides the merchant with a merchant account to accept payments. The payment gateway sends transaction data to the acquiring bank, which processes it and forwards it to the issuing bank (the customer’s bank). The acquiring bank ensures that the merchant receives the funds once the transaction is authorized and completed.