Introduction

The digital revolution has transformed how we make purchases and conduct business. At the heart of this transformation are payment gateways – secure tools that authorize and process transactions across multiple channels. Whether you’re a merchant or a customer, understanding payment gateway terminology is essential. This A to Z guide will walk you through the key concepts, tools, and technologies powering today’s seamless, secure, and efficient payment systems.

A

API Integration

API integration is the backbone of modern payment gateways. It allows websites, mobile apps, and software platforms to communicate directly with the payment system in real-time. This enables businesses to accept and process payments in an uninterrupted process without redirecting users to third-party hosted sites. All this is to foster a seamless user experience, faster processing of transactions, and a greater degree of customization for developers.

Analytics & Reporting

Analytics and reporting tools are among the most important features of payment gateways that provide merchants with actionable insights. These tools track sales performance, monitor volumes of transactions, and identify customer behavior, and detecting anomalies or trends to identify potential fraud or optimization areas.. They provide detailed reports and data visualization so that businesses can make decisions that will help them optimize their payment processes to enhance revenue generation.

Auto-Reconciliation

Auto-reconciliation is a time-saving feature that matches incoming payments automatically with invoices or other orders. Thus, the process eliminates any need for manual checks, diminishing the risk of error or mismatch. As for the automatic reconciliation, it streamlines the entire accounting process quickly, assuring all payments are accurately captured with the easy spotting of discrepancies.

Acquirer Reference Number (ARN)

Acquirer Reference Number (ARN) is a unique identifier assigned for a card transaction at the moment of its processing by the acquiring bank. It serves as a means for the merchant and the customer to track the status of a transaction ever since its inception, especially with refund or chargeback cases. ARNs are typically required for customer care representatives to quickly troubleshoot payment-related issues.

Address Verification Service (AVS)

The Address Verification Service (AVS) combats fraud by verifying a credit cardholder’s billing address supplied in a transaction. By matching the address supplied with the one registered with the issuing bank, AVS can help identify a possibly fraudulent transaction. It is widely used for online or card-not-present payments for added security.

Authorization

Authorization describes the process whereby a card issuer (usually a bank) approves or rejects transactions after passing several checks, including card validity, availability of funds, and fraud indicators. This is a very important step and occurs in real-time before a payment settles. While a successful authorization means a transaction is approved, the funds are only reserved, not yet transferred.

Automated Teller Machine (ATM)

Automated Teller Machine – an electronic banking outlet that allows users to withdraw cash, check account balances, and, sometimes, to deposit money. While ATMs are not part of online payment gateways, they are part of the broader digital payment infrastructure, particularly for card networks and withdrawals. They are widely used for cash transactions and other banking services that complement online payments.

Anti-Money Laundering (AML)

AML (Anti-Money Laundering) refers to the set of laws, regulations, and procedures aimed at preventing money laundering and other financial crimes. The regulation requires that payment gateways invest in identity verification, transaction monitoring, and reporting of suspicious activity to comply with AML. It is these measures that would ensure that the payment ecosystem is kept secure and transparent.

B

Bank

A bank is a financial institution that plays a central role in the payment gateway ecosystem. Banks issue payment cards, acquire transactions on behalf of merchants, and securely manage the movement of funds. However, banks keep it all moving around safety-wise, and thus, all necessary measurable financial regulations apply to the infrastructure set for a bank, which provides services for local as well as foreign transactions.

Batch Processing

A method where multiple transactions are grouped together and processed at once, usually at the end of the business day. Common in settlement cycles and reconciliation.

Billing

Usually, billing means invoices raised against the purchase of goods or services. Billing features may include invoicing, subscription billing, and automatic reminders, helping reduce errors and improve cash flow. Well-billed is when bills have efficiently reduced human error, improved cash flow, and created a happy customer with timely reminders as well as clarity.

Beneficiary

Beneficiary or payee refers to the person on behalf of whom a transaction has been finally processed. In the merchant transactions, the beneficiary is the concerned business or seller. Payment gateways ensure that the payment will route correctly into the final beneficiary’s account with full traceability and transparency. It is of utmost importance in complex business environments with a multitude of contributors.

BNPL (Buy Now Pay Later)

BNPL (Buy Now Pay Later) allows customers to defer payments while merchants receive full payment upfront. Integrated BNPL solutions in payment gateways help boost conversions and offer flexible financing at checkout. BNPL scheme functionality integrated within payment gateways enables customers to access flexible credit solutions at the time of checkout.

Batch

Batch processing is combining multiple transactions and processing them together at a preset time. The trend in batch processing is mostly being adopted by high-volume merchants, particularly in cases of periodical payments and settlements. Batch processing refers to handling multiple transactions at once, typically used for payroll, settlements, or vendor disbursements in B2B payments.

Bill Pay

To most, Bill Pay means using a payment gateway to settle their periodic outflows of cash for things like utilities, subscriptions, insurance, or phone services. A typical Bill Pay system includes a scheduled payment, a reminder, and several payment methods to let a person manage the collection of money each month better through bank or third-party platforms integrated with gateways without defaulting on a payment.

Breach

A breach in payment systems refers to the unauthorized infiltration of sensitive data such as card numbers and personal or financial records. Such conduct, in the end, may lead to loss of finances, legal liabilities, and severe tarnishing of the reputation of the company. Payment gateways have instated robust security features such as tokenization, encryption, and fraud detection instruments, both to avoid a breach and inspire confidence in customers.

C

Card Issuer

The card issuer refers to a bank or financial institution that issues debit or credit cards to users and is a possible approving or disapproving source on transactions, adds credit limits, and services the user’s account. The card issuer runs with the payment gateway and acquirer to provide quick and secure transactions.

Cardholder

A cardholder is the person who possesses and uses his or her credit or debit card to make purchases. The cardholder initiates the payment when the card is used on the merchant site, mobile app, or point-of-sale terminal. Every payment gateway checks the credentials of the cardholder regarding transaction verification and processes immediately to block any fraud or unauthorized usage.

Chargeback Protection

Chargeback protection refers to its service to helps merchants fight disputes and reduce losses from chargebacks. It is an umbrella for transaction monitoring and fraud detection, and fighting bogus claims. It gives merchants peace of mind by enabling them to reduce the customer’s cost of bringing a dispute or starting an inquiry-related refund.

Chargeback

Chargeback means that a charge the customer disputes, and the card issuer credits that amount back to the customer’s account. The dispute may arise from unauthorized use, dissatisfaction with a product, or incorrect billing. Given the threat that chargebacks pose to the merchant’s revenue and reputation, payment gateways do have mechanisms to detect those disputes and allow enough time for the merchant to mitigate the damage.

Contactless Payments

Contactless payments are based on near-field communication (NFC) technology to allow consumers to make purchases via the simple tapping of their card, smartphone, or wearable device onto a terminal. They are fast, convenient, and secure, which is why contactless payments have gained popularity in the retail and transport sectors. Payment gateways facilitating contactless transactions now have to pay attention to the emerging consumer preference for convenience in transactions.

Credit Card

Credit cards leverage money borrowed from the banks for purchases, which allows the individual to pay back later. If not paid on time, credit card balances may incur interest charges or late fees. Credit cards are among the most accepted methods of obtaining goods and services on the Internet. Generally, when it comes to credit card transaction processing, payment gateways ensure secure authorization, data encryption, and PCI-DSS compliance.

COD (Cash on Delivery)

Cash on Delivery ordinarily defines the mode of making a payment where the payment for an item or a service is made by the buyer at the time of delivery, rather than during online checkout. This act would give much privilege to customers preferring cash, while it would be a difficult task for the vendors’ business line concerning logistics, not to mention fraud. Payment gateways supporting COD may include reconciliation tools for delivery confirmations and payment tracking.

Commercial Payment

Commercial Payments are called such because they refer to transactions between businesses or from businesses to vendors in return for their services or products, or infrastructure. They may include bulk payments, invoice settlements, vendor disbursement, etc. Commercial payments facilitate the exchange of money between businesses. They require payment gateways with high transaction limits, a detailed audit trail, integration with accounting systems, or both.

Cross-Border Payments

Cross-border payment consists of a transaction in which money is transferred between the accounts of parties located in one country and another. The dealings here are usually subject to currency conversion, international fees, and regulatory compliance. Beyond this, payment gateways supporting cross-border transactions are expected to take part in dealing with several currencies at once, comply with local laws, and provide very competitive exchange rates and fast settlement options. They often require integration with FX (foreign exchange) services and compliance with AML/KYC norms.

D

Digital Payment

A digital payment is an electronic transaction without either the actual currency or a paper-based check. Payment would, therefore, be via debit or credit cards, a mobile wallet, the internet, or a UPI. It promises convenience, speed, and security, besides improving business operation performance in transaction tracking. Indeed, economies will increasingly move to cashless models, thus making digital payment the very current backbone of commerce, as it is online and offline.

DCC- Dynamic Currency Conversion

Dynamic currency conversion allows an international customer to buy a product or service in their currency while being in a different country. It thus provides a live exchange rate with an option for either currency at the point of transaction sale or while purchasing over the internet, increases the customer’s experience as far as the merchant is concerned for future purchases with that user, because of the transparency it offers in the pricing. While convenient, DCC may result in less favorable exchange rates compared to those offered by banks.

Debit Card Payment

When the purchase is made, the customer withdraws cash from his/her bank account. As to borrowing, this method lends itself less than a credit card; hence, a user on a budget would prefer it. Payment gateways involve verifying account details for debit card payments, ensuring security during the transaction, and timely transfer of funds to the merchant.

Deposit

A deposit is placing money in a bank account. In the payment context, a deposit may refer to either an advance payment by a customer or the settlement amount credited to a merchant’s account post-transaction. Thus, efficient management of deposits also becomes relevant to cash flow management for businesses.

Discount Rate

The discount rate is the percentage a merchant pays to banking providers or the payment processor for accepting card-based payments. It is often a percentage of the transaction sum and is varied depending on many factors, including the type of card used for payment, transaction volume, and the risk profile of the business. This is even more important than a merchant’s expense when it comes to selecting a specific payment gateway; the lower the discount rate, the lower the expense.

E

Electronic Funds Transfer

The transfer of money between banks electronically is called Electronic Funds Transfer (EFT). Direct deposits, online transfers through the internet, and ATM transfers are some examples. EFT systems are fast, fairly regulated, and greatly mitigated by any human handling of funds. In this sense, payment gateways ensure secure yet strong and efficient transfer of funds among customers, merchants, and banks.

End-to-End Encryption

Very securely, this would be an E2EE measure that secures the data transaction. The payment data is encrypted at the sender’s end and is decoded at the receiver’s end only. That way, the sensitive information will not be accessed by intermediaries, such as payment processors and internet service providers. E2EE protects the customers’ data from being compromised and fraudulent conduct; therefore, it builds trustworthiness in digital payments.

EMI Payment (Equated Monthly Installments)

The EMI payment facility allows customers to procure large items for smaller monthly payments. EMI options are often offered by banks and card issuers by integrating them with the payment gateway during checkout. EMI schemes reduce the cost of high-ticket products to the consumers while making them sell faster for the merchants. Payment gateways usually show EMI schemes at checkout, allowing consumers the freedom of choosing a monthly installment that suits their budget.

Embedded Payments

Embedded payments provide a seamless payment experience directly built into a software or platform so that the user does not have to switch to any other app or interface. For example, booking a cab, ordering food, or subscribing to any service in one app uses embedded payments. These kinds of solutions work best for enhancing customer convenience, reducing friction, and improving business conversion rates.

Electronic Payment

Electronic payments are non-cash, digital transactions made on any platform, be it credit or debit cards, mobile wallets, UPI, net banking, or NFC-enabled payments. Electronic payments are fast, traceable, and safer than cash and support remote transactions that promote contactless methods. They also form a basis for modern commerce, both online and offline.

F

Full-Service Payment Service Providers

The full-service payment service providers are end-to-end payment solution providers that play the role of payment collection, fund settlement, and reporting. They support multiple payment methods, fraud protection, chargeback handling, reconciliation tools, and easy integration with e-commerce platforms or POS systems. They eliminate the need for merchants to negotiate terms with multiple vendors, hence providing a smoother and more cost-effective experience.

Frictionless Payments

These frictionless payments are transactions designed for maximum ease and convenience. Examples include one-click checkouts, auto-filled payment details, biometric authentication, and contactless payments. The decrease in steps in the payment process increases conversion rates and customer satisfaction. Payment gateways that focus on frictionless payments are a big plus for merchants in augmenting user experience and sales performance.

Fraud Detection

The act of fraud detection uses algorithms, machine learning, and real-time monitoring to identify suspicious behavior in some payment systems. Most modern gateways have built-in fraud detection mechanisms programmed to flag transactions that appear to be out of the ordinary, as assessed against a predefined set of criteria such as location, behavioral patterns, and transaction history. These systems essentially protect merchants and consumers against actual financial loss and lend credibility and trust to online transactions. These systems continuously evolve with machine learning to adapt to new fraud tactics.

Fast Payment Gateway

Speed is of vital importance in the present-day digital world, and with a fast payment gateway, thriving transactions can be completed rapidly without delays. It needs to have fast authorization, instant payment confirmation, and rapid fund settlements. The speed of a gateway adds to the reduced cart-abandonment rates and increases customer satisfaction-facilitated shopping, sales, or any other significant sales.

Fingerprint Authentication

Fingerprint authentication is a biometric feature in digital payments that enables payments using mobile devices. Such authentication will check the print of the user’s fingerprint, thereby limiting transactions to a certain level only to authorized users. This is to enhance security and convenience while dealing with what is accomplished in saving passwords or OTPs. This gives a modern touch and user experience to many apps and payment platforms today.

Funding Settlement System

Fund settlement is the last part of a payment transaction, when the money is transferred from the payer’s account to that of the beneficiary. A settlement system, in the payment gateways, is used to calculate the funds to be disbursed to the merchant after considering all the charges and chargebacks incurred. Fund settlement systems are very efficient in disbursing timely manner and facilitating cash flow for businesses. Delayed settlements can affect business cash flow, so optimized systems are key for merchant satisfaction.

Failed Transaction

A failed transaction typically means that a particular payment attempt has not materialized as follows: a) insufficient funds on the account, b) technical failure of processing the card (expired), c) incorrect filled details. Such failures can frustrate customers and cause a loss of sales. Payment gateways minimize the incidence of failed transactions by real-time validations for attempts by payment retry mechanisms, reporting tools on errors to inform users, and other strategies intended to improve success rates.

G

Geo-location

Geo-location technology harnesses GPS or IP address data to ascertain a user’s physical location. Within digital payments, it serves the most critical purpose of improving security and fraud detection. For instance, let us assume that a card issued in India is suddenly used for a purchase from another country within minutes. In that case, the system can flag the transaction as suspicious. Payment gateways can thus compare the location of the transaction with known locations of the user to reduce chances for unauthorized access and fraudulent transactions.

Guaranteed Payment

Guaranteed payment means that the merchant is guaranteed to receive the transaction amount once the payment has been approved by the card issuer or bank. This is especially useful for high-risk transactions or industries with high chargeback and cancellation threats. Thus, merchants are assured of financial security, and confidence in digital commerce transactions is increased.

Gateway Fee

The gateway fee is the charge of a payment gateway provider for processing transactions on behalf of the merchant. The fee is generally a small percentage of the transaction amount or a fixed fee per transaction. It encompasses infrastructure, fraud detection tools, maintenance, and integration support. Transparent gateway fees allow businesses to make decisions based on the cost the provider takes per transaction, compared to their transaction volume and business model.

Google Pay

Google Pay is a renowned digital wallet and an online payment platform developed by Google. Using Google Pay, the user can make the payments either from their mobile, linked bank accounts, or cards. Google Pay facilitates peer-to-peer transfer and merchant payments, making it a favorite for many everyday use cases. The payment processing is secured with tokenization and encryption, with a very easy and smooth integration with many payment gateway systems.

Government Payment Portals

Governments operate designated payment platforms for citizens to make online payments for service fees rendered by the government; for example, taxes, licenses, utility bills, or fines. The payment gateways are integrated into such portals to ensure that public money transactions are safe, transparent, and efficient. These portals also usually offer several payment options with instant receipt generation for accountability.

Gateway Downtime

Gateway downtime means times when the payment gateway can be said to work with failing signs. Such down times are caused by technical maintenance, server problems, and cyberattacks. Users could be unable to transact during downtime, which could lead to a loss of revenue and dissatisfaction among customers. Reputedly, a Gateway provides an uptime guarantee along with alarms to effectively reduce and handle such occurrences. Top-tier gateways often provide 99.9 %+ uptime SLA (Service Level Agreement).

Gateway Transaction Logs

These are complete, detailed records of all transactions that pass through a payment gateway. Generally, the logs contain transaction IDs, timestamps, user details with payment amounts, status-success or failure-and error messages. The logs can be used for various auditing activities, troubleshooting, reconciliation, and fraud investigations. Many payment gateways provide dashboards for real-time access and analysis of such logs.

H

Hosted Payment Page

A hosted payments page is a secure webpage of a payment gateway where customers go to finalize a transaction. The main advantage of this is that it alleviates the burden of PCI-DSS compliance from the merchant since no secure data is processed in the merchant’s servers, but rather in the payment gateway. Hosted pages are customizable, mobile-ready, and encrypted for secure payments.

Hosted Invoice Payments

Hosted invoice payments send out digital invoices to customers containing a direct link to pay. When the user clicks on the link, he/she is taken to a secure page to be able to complete the transaction using various ways to pay. It boosts the collection of payments while still keeping it safe, especially for businesses that are service-based, freelancers, or have a subscription service.

HSA Payment Gateway

HSAs, or Health Savings Accounts, let users pay out-of-pocket medical expenses using their HSA debit cards. This architecture ensures compliance by ensuring that all expenditures on health care are included, both from the standpoint of billing for clinics, hospitals, and pharmacies. Such gateways promise easy integration with health service providers and a streamlined patient experience regarding payments.

Hosted Tokenization Gateway

This type of gateway replaces sensitive customer information, such as card numbers, with a secure and unique token. Tokenization prevents the actual payment details from ever being stored on the merchant’s systems, thus minimizing the potential data breach risks. Hosted tokenization gateways execute the entire process off-site, allowing merchants to enjoy superb security and PCI compliance advantages.

I

Integrated Payment Gateway

An integrated payment gateway is a payment system that is already in place in a merchant site or app, allowing customers to transact without switching to another web page. It gives a merchandiser a branded and integrated checkout experience, which usually means higher conversion rates. Integration means that a very strong, technical implementation is expected of the system, but the merchant will have absolute control over the interface and payment flow.

Interactive Voice Response( IVR ) Payment

IVR technology allows a customer to make secure payments over the telephone via a computerized interactive voice response system. The customer keys in the required payment-intended information using the phone keypad, and the system processes the transaction in real-time. It is commonly used for utility bill payments, subscription renewals, and order confirmations where users have a lack of Internet access.

Instant Bank Transfer

An instant bank transfer is meant for a real-time transfer of electronic funds from one bank account to another. Unlike a traditional bank transfer, they are much faster, taking just a few seconds to complete. An instant bank transfer is often a great choice for payments that are time-critical, e.g., online purchases, peer-to-peer transfers, or emergency payments. Many payment services integrate instant bank transfer functionalities to reduce settlement time and increase customer satisfaction.

In-app Payment Integration

In-app payment enables customers to perform payment transactions within the mobile app without having to leave it. They can now order food, take a cab, or buy digital content within the app, with the payments being made on the run through their saved credentials. This streamlines the customers’ business experience because they can make their payments much quicker and more securely, and smoothly.

Invoicing and Payment Gateway

Some payment gateways offer merchant invoicing integration, which enables the merchant to raise digital invoices for clients who can pay directly. Discrete payment options exist alongside these invoices, allowing fulfillment of payments using various means, thus cutting the hassle of producing and keeping track of payment receipts from a central e-dashboard.

Interchange Fee

The interchange fee is a charge that the acquiring bank, or the merchant’s bank, pays to the issuing bank, or the customer’s card provider, for processing card transactions. It is mainly for payment processing, fraud prevention, and risk fees. The interchange fee is charged on a percentage basis on the transaction amount, upon the card and the nature of the transaction type.

International Payments

These payments are well beyond borders—currency turnovers and law compliances are instant steps in compliance with worldwide banking regulations. If payment gateways help international payments, businesses will take payments from clients throughout the world; these payments shall arrange the conversion rates, taxes, charges, and compliance with regional laws. In this way, global commerce becomes accessible.

J

Just-in-Time Funding

JIT Funding is an innovative payment system where funds would be received to a card or an account when the payment is made. Most importantly, it does not involve preloading the funds; they are transferred in real-time at the moment of the transaction. It minimizes the potential risk that any unused funds might get stolen or misappropriated and helps companies manage their cash flows better. Mostly used in virtual cards and business expense management systems.

JWT (JSON Web Token)

A compact, URL-safe token used in secure API authentication between merchants and payment gateways, ensuring safe access and data exchange.

K

Kiosk Payment Gateway

A kiosk payment gateway allows users to make self-service payments through terminals or machines installed in public areas such as malls, hospitals, or government offices. These will allow people to make payments, recharge any services, and buy tickets via cards, UPI, or mobile wallets. The gateway is responsible for ensuring real-time payment processing and transaction security, and helping the end-user’s convenience in an area where there is limited human assistance.

Know Your Customer (KYC)

KYC refers to the verification of identity process that is compulsory by financial institutions and payment platforms in verifying the client’s identity. This process collects documents like ID proof, address proof, and sometimes collects biometrics. KYC is done to prevent the occurrence of fraud, money laundering, and any illicit activities, as it ensures that dealings are made by valid entities using their real identities.

Kickstart Payment Integration

Kickstart payment integration refers to plug-and-play or quick-start solution capabilities by a payment gateway that is offered to clients so that businesses require the least coding exercises possible to have the company’s backend set up with payment systems. Available tools generally also include readily available, prebuilt templates, sandbox environments, and guides to fasten deployment of secure, functional payments flows-suitable for new businesses or small enterprises in a hurry to launch online.

L

Local Payment Methods

Popular and specific payment options in a certain region or country, such as UPI in India, iDEAL in the Netherlands, or Boleto in Brazil, are local payment methods. Payment gateways that support local ones have improved rates of conversion as they serve users with their preferred payment mode, thus improving trust and accessibility to domestic markets.

Late Payment Fee

A late payment fee is charged on customers who do not pay on or before the due date. It is mostly applicable in subscription billing, repayments of loans, or prepaid utilities. Within payment gateways, automated systems may compute and apply late fees, send reminders to respective debtors, or generate updated invoices to ensure the collections are made on time.

Ledger

A record that tracks all credits and debits associated with merchant transactions in a payment gateway system, useful for settlements and audits.

Low-cost payment Processor

A low-cost payment processor provides all such services that are required by a payment gateway with the least amount of cost involved for transaction charges, including the set-up costs. These are for small businesses, start-ups, or single sellers who want payment processing without much expense on extra features. Generally, pay-as-you-go modes will be there along with easy onboarding.

Link-Based Payment Gateway

This function allows businesses to create a unique payment link that can be shared via SMS, email, or social media. The customer can click on the link and make the payment without requiring a website or app. Link-based gateways are typically used by freelancers, service providers, and small vendors for fast and safe collections.

Lock Box

A lock box is a service provided by the bank for receiving customer payments, such as checks or remittance slips, at a secure mailing address. The bank picks up, processes, and deposits the payment directly into the merchant’s account. This system speeds up collections, reduces manual handling, and improves cash flow for businesses having a very large amount of paper-based payments.

M

Monthly Subscription Payment

It is a recurring payment in which customers are charged automatically each month for the service or access to product(s) such as streaming platforms, software tools, or memberships. Subscription billing-enabled payment gateways handle recurring charges, retry automatically on failures, and send reminders to ease revenue management.

Merchant Account

Merchant accounts are business accounts opened with a bank to facilitate the acceptance of card payments by the merchant from customers. Money from card sales is first paid into this account and then transferred to the merchant’s main account. It acts as a holding account; it is a must for accepting electronic payments using a gateway.

Multi-Currency Support

Multi-currency support allows the merchant to accept payments in diverse international currencies. This feature is essential for e-commerce operations with global reach since it allows customers to shop in a currency that suits them. Payment gateways with multi-currency support shoulder the burden of currency conversion, display local pricing, and facilitate international transactions smoothly.

Mobile Payments

Mobile payment is a method of transaction where a purchase is completed using a smartphone or wearable device. This includes an app-based payment through scanning QR codes, which Spring wallets (Apple Pay, Google Pay) or UPI. Mobile payments provide convenience, speed, and security, making them more desirable among customers every day.

Marketplace

A marketplace is an online platform for many sellers or vendors to list and sell products or services to customers. Examples include Amazon, Etsy, and Flipkart. The payment gateways for marketplaces support split payments, commission management, refunds, and KYC for each vendor.

MID (Merchant Identification Number)

MID is a distinctive profile number specifically issued for the identification of any merchant by its bank or clearing aggregator, used for the monitoring of all activities that unfold within the merchant’s account. It assists in creating reports, auditing transactions for accuracy, and scrutinizing merchant-specific activity.

Merchant Discount Rate (MDR)

MDR is a fee paid to the payment processors by the merchant for each processed card transaction. A percentage of the transaction amount is typically the discount that is paid for the processing itself and the protection of fraud and infrastructure provided by the processor. MDR rates are based on company size, transaction volume, and industry.

Multi-Factor Authentication (MFA)

Multi-Factor Authentication (MFA) is a security mechanism that requires users to verify their identity using two or more independent factors before granting access to a system or completing a transaction. These factors typically fall into one of three categories:

- Something you know – like a password or PIN

- Something you have – such as a mobile device or a one-time password (OTP)

- Something you are – including biometrics like a fingerprint or facial recognition

By combining multiple layers of authentication, MFA significantly reduces the risk of unauthorized access, even if one of the factors (like a password) is compromised. It’s widely used across sectors today to enhance digital security for everything from banking transactions to school systems and enterprise platforms.

Mobile SDK (Software Development Kit)

Mobile SDK is a software toolkit that has been created by payment gateways to enable developers to easily and seamlessly incorporate payment functions into their mobile applications. SDKs consist of prebuilt components for checkout processes, card scanning, and fraud identification and encryption to provide the customers of the application with a safe and compliant payment process.

N

Net Settlement

Net settlement indicates the net amount transferred between financial institutions after all credits, debits, fees, and adjustments have been accounted for. The point of the payment system is to process a batch of multiple transactions throughout the day and calculate the final net amount transferred at the end of the day. This means reduces transaction volume and helps achieve efficient liquidity management for financial institutions.

Net Banking

Net banking, also known as internet banking, permits patrons to access their accounts online and get a slew of services, from transferring money and paying bills to checking the balance. It’s a decent, secure way for businesses and individuals to regulate their financial needs by typing in the bank URL, but without visiting the bank directly.

Network Fee

A network fee is a fee charged by a payment card network (e.g., Visa, MasterCard, RuPay) for routing and processing transactions. This fee goes toward the maintenance of the infrastructure of the payment network and ensures that the transactions are secure and smooth. By all reports, it is a part of the overall processing costs of most transactions, borne by the merchant.

O

Online Payment

Online payment refers to a transaction method carried out over the internet, connecting with electronic payment methods, including credit/debit cards, net banking, mobile wallets, or UPI. It means that the customer makes an online payment to purchase a product or service, avoiding the use of cash. What people appreciate is that buying can be facilitated without any effort. Quick online transactions are what make them so popular, with flexibility, speedy transactions, and the possibility from any place with an Internet connection.

One-click Checkout

One-click checkout gives customers the ease of purchasing with only the push of a button using saved payment and shipping details. It eases the friction-creating poundage in the mind of the buyers during checkout and, therefore, very strongly improves conversion by a nice and smooth buyer experience, especially for the ex-buyers.

OTP Authentication

OTP or one-time authentication measure is a stateful online transaction to verify the identity of the customer. OTP may be a treasure key for another type of fraud typing into a cell phone or an email, or a push notification together to authenticate a transaction. This additional layer of the device can protect it from fraud.

Omnichannel Payment Solution

The omnichannel payment solution continues to be one great way to allow businesses to collect and reconcile payments on different platforms – through online stores, mobile apps, store cash registers, etc., while keeping the backend reporting consistent. So, no matter how customers prefer to shop, they can be subject to a consistent and hugely flexible payment experience.

P

Payment Processing

Payment processing is the whole process of handling a financial transaction-from prompting a payment, validating customer details such as card information and authentication credentials. Payment processing entities act as providers behind the curtain, ensuring accuracy, security, and timely settlement.

Payment Reminder

A payment reminder is an automatic communication sent to remind the customer to pay for an upcoming payment or debt. As such, a payment reminder is both a deterrent to late payments and an enhancer of cash flow for businesses. The reminder might be in the form of SMS, Email, or In-app notifications that usually include a direct payment link to simplify the process.

Payment Reconciliation

Payment reconciliation refers to the comparison of internal records of transactions with statements and reports from external sources, such as banks or gateways, to verify that all payments have been accurately received and recorded. Thus, discrepancies can be identified, lost or pending funds can be traced, and accurate financial records can be maintained.

Payout

The process of disbursing funds from a merchant’s payment gateway account to their linked bank account. Payouts can be scheduled at fixed intervals or triggered instantly, ensuring timely access to revenue and smooth cash flow management for businesses.

PCI DSS Compliant

PCI DSS, which is short for Payment Card Industry Data Security Standard, specifies that the payment mechanisms and methods used by companies must adhere to security standards set by the PCI Security Standards Council to protect cardholder data.. Using a PCI-compliant payment mechanism secures the company from data breaches and helps avoid penalties and legal issues.

Payment Link

Payment link created through a payment gateway usually generates a unique URL that can be forwarded to customers and request a payment. Once the URL is opened, the user is directed to a secure page where the transaction can be completed through different means. This suits freelancers, small businesses, and customer support teams alike.

Payment Gateway

A digital service that firmly moves payment data between customers, merchants, and financial institutions, facilitating online and electronic transactions, is referred to as an online payment gateway. It handles authorization, processing, and completion of transactions with robust security and regulatory compliance.

Payer

Payer is the person or organization that creates and approves a payment transaction. The fund is made available by the payer to complete the purchase or pay the bill, which can be done using various methods, including cards, bank transfers, UPI, and wallets.

POS Payment Gateway

A POS payment gateway is the one used in physical trading or service environments to conduct payments through a card using a card-swiping machine or terminal attached to a computer. POS gateways often support pre-authorization and various payment methods such as credit/debit cards and digital wallets, generating printed or digital receipts instantly.

Q

QR Code

A QR code (Quick Response code) is a type of two-dimensional barcode that stores data in a machine-readable format. When scanned using a smartphone or compatible device, it can instantly provide information or trigger actions—such as opening a link or initiating a payment.

In the world of digital payments, QR codes are widely used for fast, contactless transactions via UPI, digital wallets, and mobile banking apps. By simply scanning a QR code, users can make secure payments within seconds—eliminating the need for cash, cards, or manual inputs.

R

Reconciliation Report

A reconciliation report is a type of financial document that helps businesses match all payment transactions with the bank records, which indicates mismatches, pending settlements, or failed payments. Such reports help in accounting accuracy, pointing out discrepancies, and smooth financial audits.

Risk Management

Risk management of payments involves the identification, assessment, and prevention of risks in the context of fraudulent transactions, chargebacks, data breach offenses, and operational failures. Good systems will therefore involve the use of tools such as fraud detection algorithms, encryption, and compliance protocols to safeguard customer data and corporate interests.

Real-time Payment Monitoring

Real-time monitoring of payments means keeping track of live transactions as they happen. This allows businesses and payment providers to detect issues such as fraud, transaction failures, or latency, enabling rapid resolution and improved customer experience.

Recurring Payments

Recurring payments are automated payment processes done at regular intervals (monthly, quarterly, yearly) for subscriptions or memberships. Once the first payment is authorized, the system will automatically debit the payer’s account without requiring manual intervention each time.

Refund Processing Gateway

A refund processing gateway allows merchants to return money to customers when an order is canceled, products are returned, or transaction processing falls into error. It is, thereby, a secure, timely, and traceable method of refunding money directly to the original mode of payment.

Retry Logic

Retry logic is an automated mechanism that reattempts failed transactions, especially those declined due to network errors or temporary bank issues. Commonly used in subscription billing or recurring payments, it increases payment success rates and ensures a smoother customer experience without requiring manual intervention.

S

SaaS Payment Integration

SaaS (Software-as-a-Service) payment integration is a feature that allows payment gateways to be incorporated within cloud-based software platforms. This, in turn, enables businesses to provide the billing, subscription, and payment collection functions directly through their software interface, making payment management more seamless for users and boosting revenue for businesses.

Split Payment

A split payment refers to the division of a single transaction into multiple payments to multiple recipients or payment modes. Such payments are common in marketplaces or group purchases, as they help to correctly allocate royalties among various vendors or balance amounts between gift cards, wallets, and cards.

SSL Certificate

An SSL (Secure Sockets Layer) certificate is the assurance of encrypted communication between a browser operated by an end user and the payment website. As a result, this prevents important information such as card numbers and passwords from being intercepted during the transaction process, instilling trust and safety in making online payments.

Surcharge

A surcharge is a fee that is added to the transaction amount, which usually covers the cost of processing the payment. Companies may impose surcharges on credit card payments to counterbalance the cost of the gateway or bank fees; however, those laws differ from one country to another.

SDK (Software Development Kit)

An SDK is a set of tools, libraries, and documentation that developers can integrate into their mobile or web applications to easily enable payment features such as card input and checkout flows. It simplifies the payment feature addition, such as checkout pages, wallets, or card input, instead of creating one from scratch.

Settlement Cycle

This means the period when a transaction is opened and the time when the funds are credited to the merchant’s account. Depending on the gateway or bank, this may range from instant settlement to a few business days.

Subscription Billing

Subscription billing is an automatic billing procedure for products and services charged to consumers, usually on a monthly or yearly basis. Subscription billing also automates renewals and helps create predictable revenue. Subscription billing is also widely used in streaming services, SaaS companies, and many fitness platforms.

T

Tokenization

Tokenization is also a very profitable way of ensuring that sensitive payment data, such as card numbers, is replaced with a random, unique identifier, a token. This token is then used to process a payment but does not expose the actual payment information, and minimizes the chances of fraudulent activities or data breaches.

Token Vault

A token vault is a secure, encrypted database maintained by a payment gateway to store payment tokens in place of sensitive card information. It enables businesses to process repeat transactions safely without exposing actual card details, thereby ensuring compliance with PCI DSS and enhancing data protection.

Transaction Fees

A transaction fee is a term for charges that are levied on the processing of payments through the gateway or card network. These include interchange fees, service provider fees, and bank charges, which are mostly paid by the merchant but occasionally borne by the customers as well.

Transaction Analytics

Transaction analytics refers to the insights generated by analyzing payment transaction data generated by analyzing payment transactions. This helps businesses to understand customer behaviors, performance metrics, trends, and make the right kinds of decisions to optimize both payment processes and revenues.

Two Factor Authentication

Two-factor authentication is a form of security by which a user must provide two identifiers before conducting a transaction. Generally, it will consist of a password and a one-time password, also sent by SMS or email to the user. This will improve security through verification against the device and the user.

Third-party Payment Gateway

A third-party payment gateway acts as an external service provider for the payment process on behalf of the company. These gateways take care of all that is involved in payment, like encryption, authorization, settlement, and compliance, and allow a company to accept virtually all modes of payment with ease and security.

U

UPI (Unified Payments Interface) Payment

UPI is a real-time payment mechanism created in India and enables people to send or receive money instantaneously on their mobile. Pay or receive payment through a number, an ID, or a QR code, making it a very easy-to-use and popular mode for peer-to-peer and business transactions.

URN (Unique Reference Number)

A URN is a certain alphanumeric number that is given to a transaction that makes it easily identifiable and can track it throughout its lifecycle. This number is usually helpful in customer support, audits, and reconciliations.

URL-based Payment Gateway

This type of payment gateway enables businesses to send out a payment request over a unique URL. When the customer clicks this link, he or she is directed to a secure payment page where the transaction can be completed. It is very useful for freelancers, those doing business via social media, and remote services.

User Authentication Gateway

User authentication gateways are responsible for authenticating the payer’s identity for transaction authorization. This may include passwords, one-time passwords (OTPs), or biometric authentication. This ensures that the transaction is valid and secure against unauthorized access.

V

VAT (Value-Added Tax)

VAT is a tax on consumption levied on goods and services at each stage of production or distribution. In the context of payment processing, VAT is charged as part of the total amount receivable by the customer from the merchant, who is then liable to remit the VAT collected to the government.

Virtual Terminal

A virtual terminal is a secure, browser-based dashboard that allows merchants to manually input and process customer card payments. Often used for phone orders, email invoicing, or remote billing, it offers flexibility to accept payments without needing physical card-swiping hardware or a storefront.

Voluntary Payment

A payment made voluntarily means free will and not under coercion. Examples include donations, tips, or prepayments, nearly always facilitated by payment gateways with flexible or custom payment options.

Void transaction

A void transaction is one where the payment is canceled before it is fully processed or settled. A void transaction cancels a payment before it is settled, meaning no funds are captured from the payer’s account.

W

Withdrawal Limit

The withdrawal limit is the maximum amount of money permissible to be withdrawn by a user from their account per day (through ATM, online banking, or use of mobile apps). These limits are incorporated to prevent fraud as well as for cash flow management.

Web-based Payment

Web-based payment refers to any payment initiated via a web browser, either on a computer or a mobile device. These transactions are mostly conducted by online banking, card entry, or UPI and are secured by the checkout systems employed at the e-commerce websites.

Website Checkout Payment

This refers to payment functionality that is directly built into the merchant’s website for securing the payment of products or services. A simplified checkout experience can significantly decrease cart abandonment and convert better.

Webhook

A webhook is an automated way of sending real-time payment event data (that is, success and failure of payment) to another application or server. This helps in the automation of processes like updating order status, sending out electronic mails, or generating invoices for the transactions.

WhatsApp Payment

WhatsApp Payment enables senders to transfer and receive money by utilizing the messaging application linked to a bank account through UPI. It is thus smooth for peer-to-peer transactions without the inconvenience of switching apps, therefore suitable for quick informal exchanges.

X

XML Gateway

XML gateway manages payment requests using XML (eXtensible Markup Language) and integrates with enterprise systems that use structured data formats for transaction processing, therefore providing a standardized way of treating complex payment instructions.

X-Payment Token

An X-payment token represents a certain kind of token that is generated by some payment gateways to represent payment credentials. It can then be stored and used for future transactions without revealing sensitive payment data.

Y

Yearly Payment Plan

A yearly payment plan is a subscription or billing model whereby the user pays once per year for access to a product or service. This type of plan is usually offered at a discount off the price of a monthly plan and is common in software and membership services.

YTD (Year-to-Date) Transactions

YTD transactions are those about the number or value of transactions completed from the beginning of a calendar or fiscal year up to the present date. This metric helps businesses track performance, forecast revenue, and assess financial health.

Z

Zero Fee Payment

Zero fee payment is concerned with transactions where the payee incurs no additional service or processing charges. This can be a selling point for the platforms, attracting users by fully promoting free digital payment avenues.

Zero Trust Architecture

Zero Trust Architecture (ZTA) is a stringent security framework where no user, device, or application is inherently trusted. Within payment systems, ZTA ensures every access request is continuously authenticated and authorized, significantly reducing the risk of fraud, data breaches, and unauthorized system intrusions.

Zip Payment Gateway

Zip is a “Buy Now, Pay Later” (BNPL) solution that allows consumers to buy a product and pay in installments, interest-free. Zip collaborates with merchants to facilitate flexible options for their customers while ensuring that the merchant is paid fully upfront.

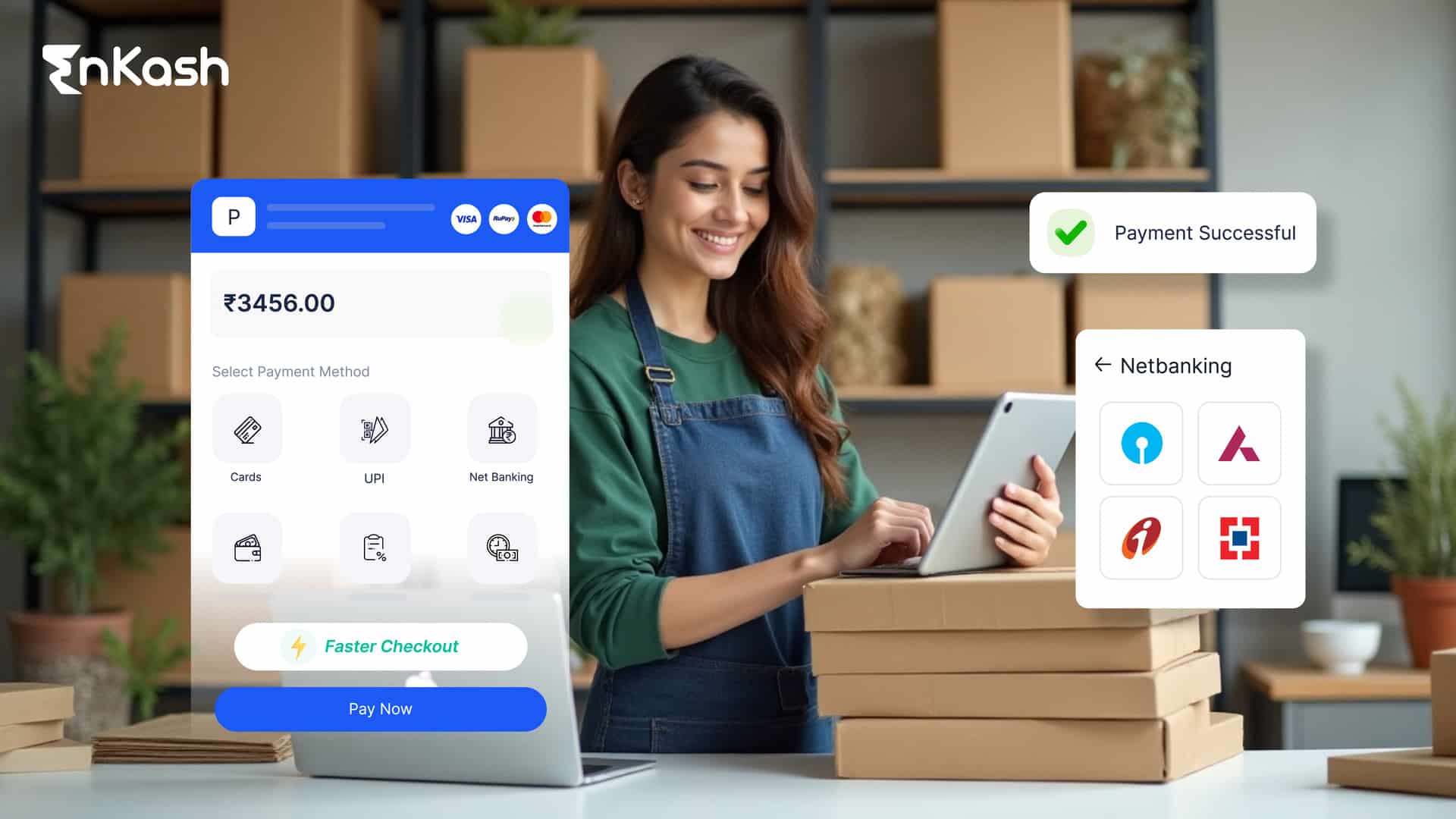

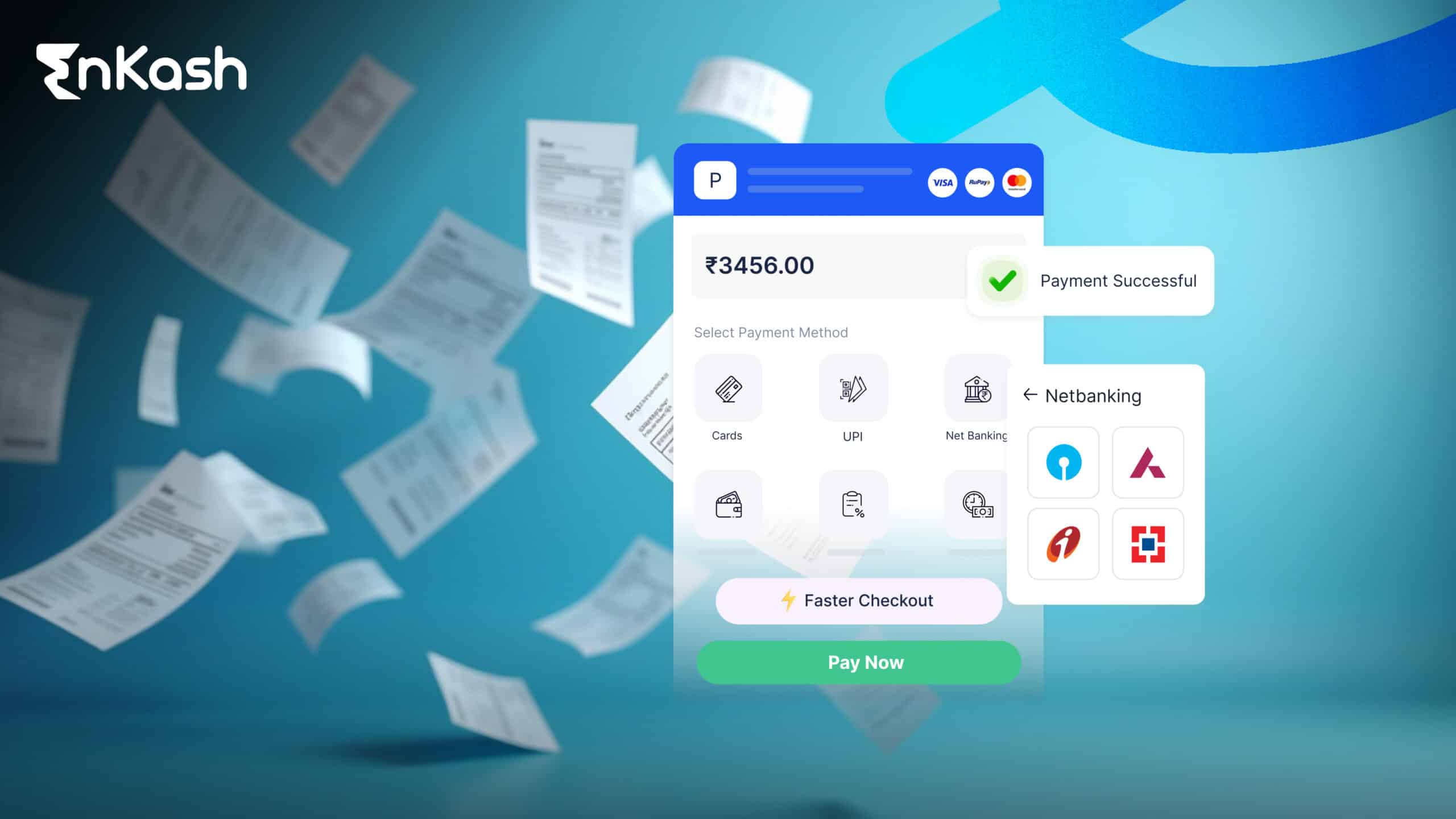

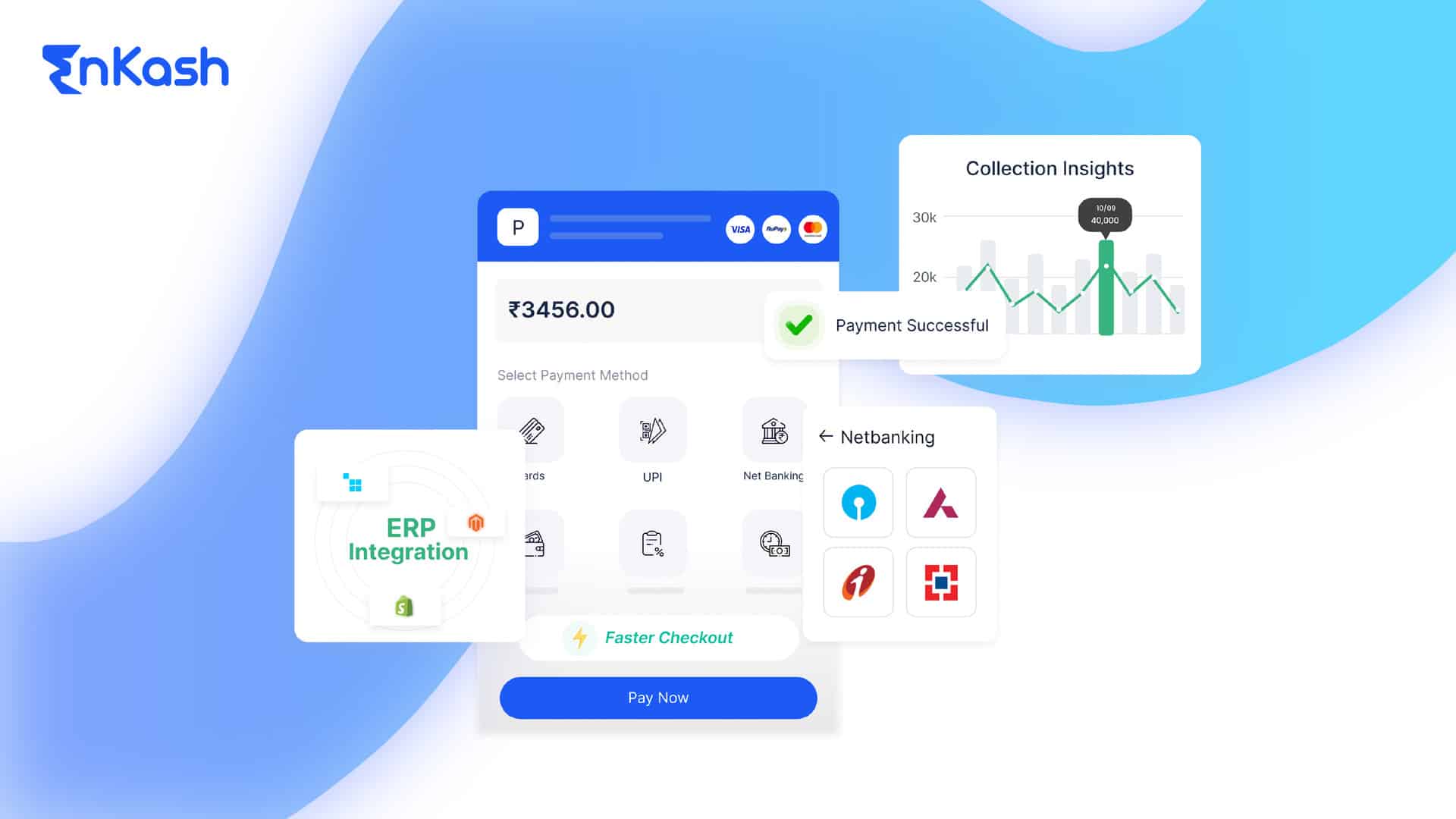

EnKash Payment Gateway

EnKash’s Payment Gateway works as a licensed online payment aggregator under the approval of the Reserve Bank of India (RBI). The payment gateway provides an efficient yet secure platform to accept different payment modes, including credit or debit cards, UPI, net banking, digital wallets, EMI, and Buy Now Pay Later (BNPL) methods. EnKash offers easy integration with flexible options through APIs, SDKs, and prebuilt plugins, which suit custom websites and platforms like WordPress and Shopify alike. The gateway provides for instant processing of transactions with active data encryption and fraud prevention measures for enhanced trust and satisfaction of the customers. EnKash also provides instant refunds and settlements that expedite the financial processes for businesses.

Conclusion

The payment gateway ecosystem is a dynamic interplay of advanced technologies, stringent regulations, and innovative solutions to ensure an efficient and safe transaction. From the simplest of QR codes to the complex backend APIs and real-time fraud detection, each component plays a crucial role. Armed with this A-Z guide, one should now have a greater understanding of the world of digital payments for businesses and consumers alike.